How Do Recent Wins or Losses Affect VC Confidence in Their Judgment

Recent wins make VCs far bolder while losses trigger deep overcaution. See how outcome bias shapes funding odds.

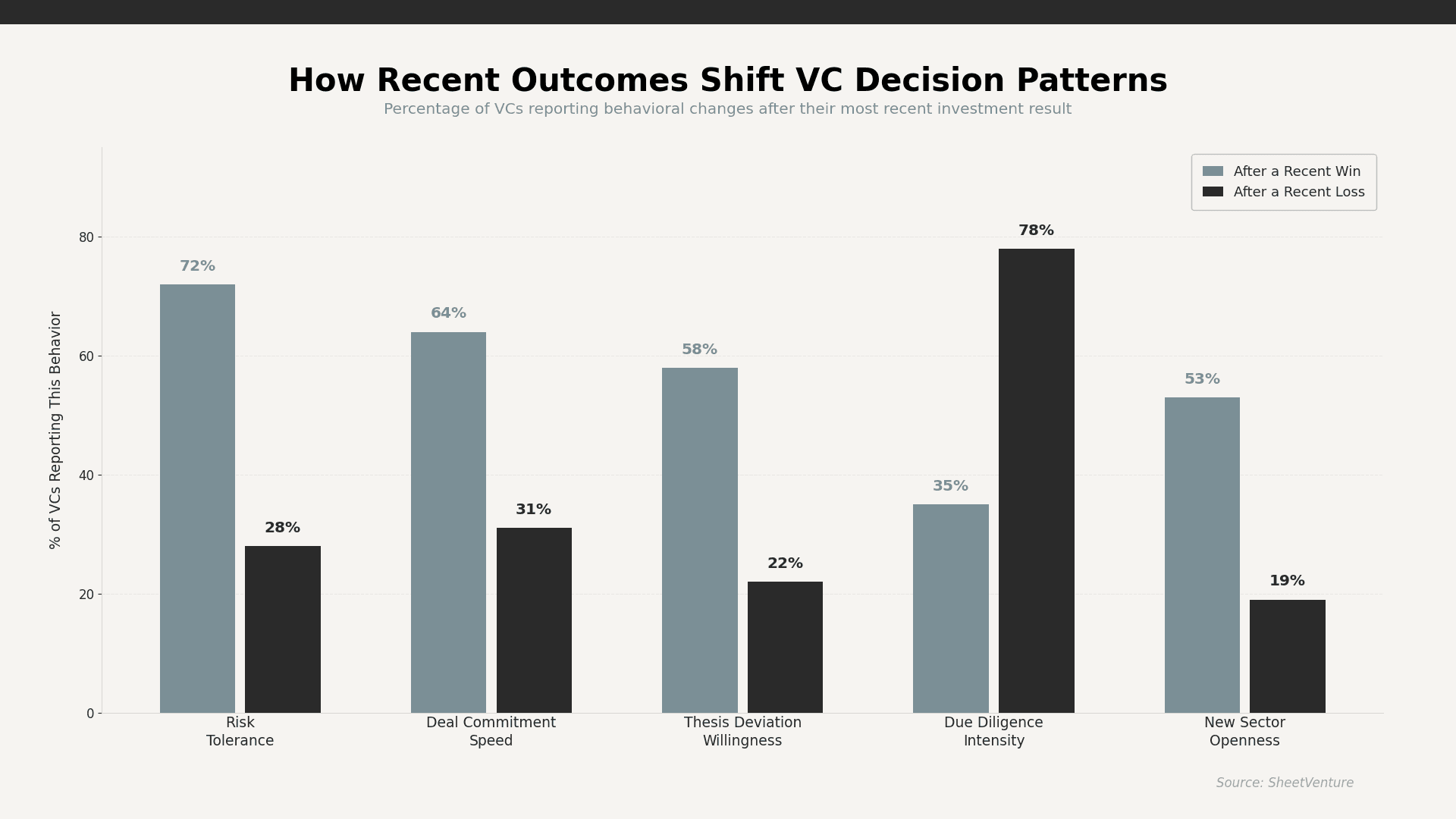

Recent wins make VCs 72% more willing to take risks on new deals. Losses increase due diligence intensity by 78%. Outcome bias quietly reshapes which startups get funded and which get passed, regardless of actual deal quality.

Venture capital runs on pattern recognition. But the patterns investors trust most are not always rational. A VC’s most recent investment outcome, whether a breakout exit or a painful write-down, directly rewires how they evaluate the next founder. This is outcome bias in action. It shapes your fundraising odds far more than your pitch deck or warm intro. Understanding this dynamic is a competitive advantage most founders overlook.

Why Do Recent Outcomes Change How VCs Evaluate Deals

Investors are human. Behavioral finance research consistently shows that recent experiences carry disproportionate weight in professional decision-making.

• A VC who just watched a portfolio company return 10x feels deeply validated in their judgment and decision process

• That validation creates shortcuts: deals resembling the winner get faster yeses and shorter diligence windows

• Conversely, a recent loss triggers defensive thinking where every risk feels amplified beyond its actual size

• The recency effect means outcomes from the last 6 to 12 months dominate how investors frame every new opportunity

This is not rational portfolio management. It is human psychology operating inside institutional capital allocation. Understanding where a VC sits in their recent outcome cycle gives founders a genuine edge. Use investor intelligence to research which VCs are in active deployment versus pullback mode.

How Do Wins Shift VC Decision-Making Behavior

A winning streak changes everything about how a VC approaches the next deal on their desk.

• Risk tolerance climbs: 72% of VCs report higher comfort with unproven business models after a recent success

• Commitment speed increases: deals that typically take 8 weeks of diligence can close in 4 to 5 weeks

• Thesis flexibility expands: 58% of VCs admit more willingness to deviate from their stated thesis after a win

• Pattern matching intensifies: founders who resemble previous winners get disproportionate attention and faster first meetings

• Check sizes grow: confidence in personal judgment translates directly into larger bets on new companies

The risk for founders is that this confidence is not really about your startup. It is about the investor’s internal narrative. A VC riding a recent win may move faster, but their conviction might be anchored in the previous deal, not yours. When investors pass on deals, the reason often traces back to their recent experience rather than your company.

What Happens to VC Judgment After Portfolio Losses

Losses hit harder than wins. Behavioral economics calls this loss aversion, and it operates powerfully inside venture firms.

• Due diligence intensity spikes: 78% of VCs tighten their evaluation standards after absorbing a write-down

• Decision timelines stretch: partners become more cautious and request additional data rounds before committing

• New sector openness drops: only 19% of VCs explore unfamiliar markets after a recent portfolio loss

• Internal firm dynamics shift: associates face heavier pushback when championing deals to the partnership

• Pass rates climb: marginal deals that might have earned a yes in better times get filtered out earlier

The same startup could receive completely different responses depending on the investor’s recent track record. Founders who sense unusual hesitation should recognize when investors lose confidence during a raise. The cause may sit entirely inside the firm, not in your pitch.

How Should Founders Use This Knowledge Strategically

Understanding the outcome bias cycle helps founders time their outreach and read investor behavior with sharper accuracy.

• Research recent portfolio exits: a VC who just celebrated a successful outcome is statistically more receptive to new deals

• Watch for thesis drift signals: investors publicly exploring new sectors may be riding post-win confidence waves

• Interpret slow processes carefully: extended timelines often reflect loss-driven caution rather than weak interest in your startup

• Understand why VCs say no: most passes reflect internal firm dynamics rather than founder shortcomings

• Build timing into your approach: target investors whose recent outcomes suggest openness and active deployment over retreat

The smartest founders build investor lists around timing and context, not just thesis fit alone.

The Bottom Line

Recent wins and losses create powerful psychological shifts in how VCs evaluate new deals. Wins inflate risk tolerance, speed up commitments, and widen thesis flexibility. Losses trigger overcaution, longer timelines, and tighter evaluation standards. Neither state reflects a purely objective judgment. Both reflect outcome bias.

Founders who understand this cycle can time outreach strategically, interpret investor signals accurately, and stop internalizing rejections that were never about their startup in the first place.

SheetVenture helps founders track real-time VC deployment activity and recent portfolio outcomes so outreach targets investors whose confidence and capital align with your fundraising window.

Publication Date: