Should I Accept Terms That Feel Slightly Unfavorable to Close My Round?

Slightly unfavorable terms can be worth accepting to close your round. Here is what founders should check first.

Sometimes yes. Whether to accept slightly unfavorable terms depends entirely on which terms, how close you are to closing, and what your alternatives look like. Some terms that sting now create small long-term costs. Others that look minor on paper can quietly destroy founder economics at exit.

The gap between "slightly uncomfortable" and "structurally harmful" is where most founders make expensive mistakes. Accepting a valuation of $500K below your target is very different from accepting participating preferred or a full ratchet anti-dilution clause.

What "Slightly Unfavorable" Usually Means in Practice

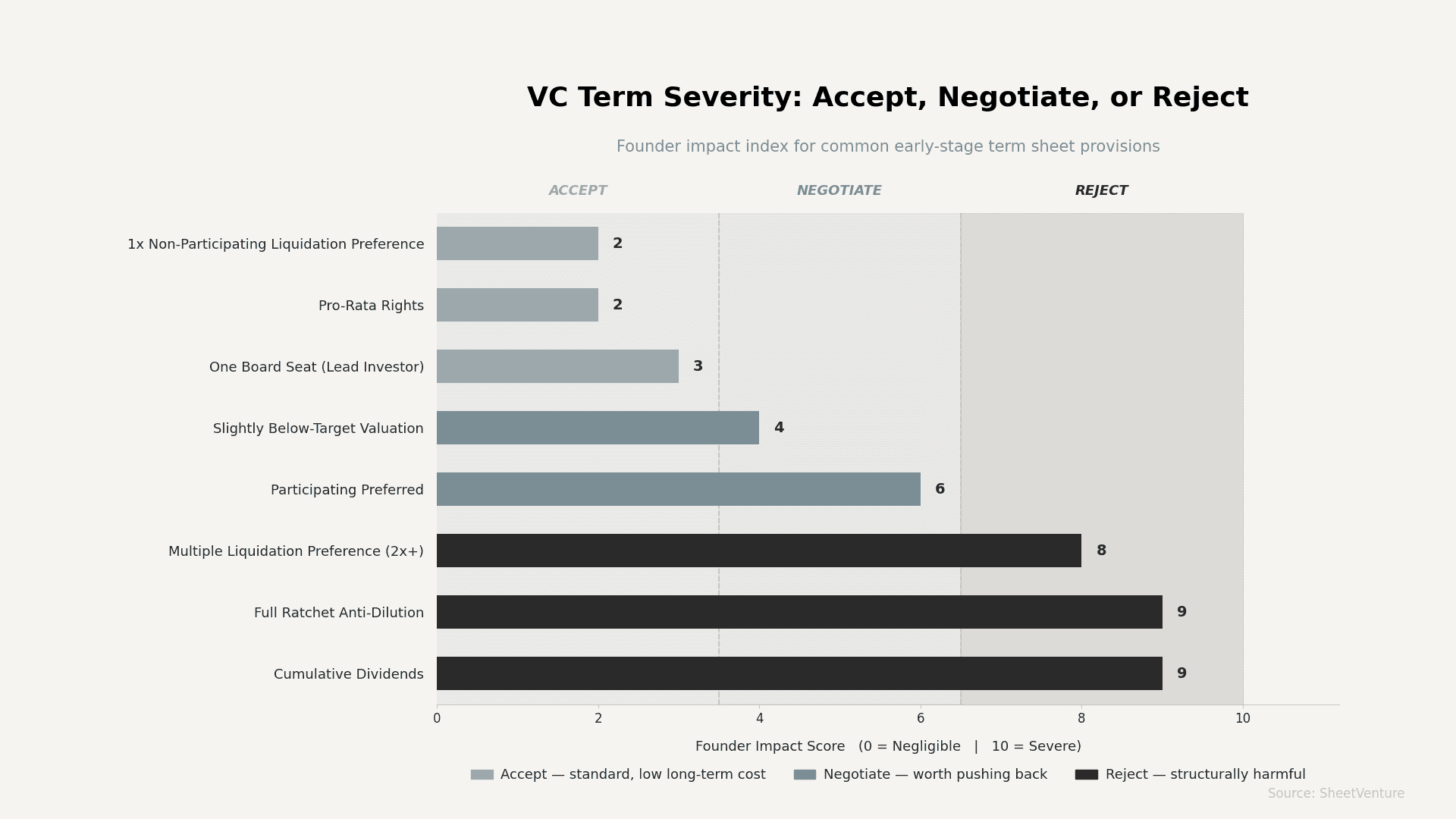

Founders tend to flag four types of discomfort when reviewing term sheets:

• Valuation lower than expected

• Liquidation preference above 1x

• Board seat going to the investor

• Pro-rata rights at future rounds

Each carries a different risk profile. One may cost you $50K at a modest exit. Another can wipe out your return entirely if the company sells below expectations.

The honest starting point: not all unfavorable terms hurt equally.

Which Terms Are Usually Worth Accepting

Some concessions affect optics more than they affect outcomes:

• Below-target valuation: A $10M vs. $12M cap hurts your paper dilution, but if the investor adds real value, the difference rarely matters by Series B. Review how valuation at seed works before anchoring too hard on a number.

• 1x non-participating liquidation preference: Standard. It protects the investor without meaningfully hurting founders at a normal exit.

• One board seat: Giving a lead investor board representation is industry-standard. The risk is in giving multiple seats to a single fund, not one.

• Pro-rata rights: These benefit the investor in future rounds but rarely cost founders direct value now.

If the term is in this category and the investor is high-quality, closing is often the right call. A funded company beats a perfectly-termed unfunded one.

Which Terms Should Make You Pause

Some provisions feel minor but compound badly:

• Participating preferred: Investors get their money back first, then participate in the remaining proceeds. At a smaller exit, this can leave founders with far less than expected. Check what signals real alignment before accepting this without negotiation.

• Multiple liquidation preference (2x or higher): Uncommon in normal markets, but some investors still ask. This one deserves a hard pushback.

• Full ratchet anti-dilution: If you raise a down round, the investor converts at the lowest price. It can devastate founder equity. Broad-based weighted average is the acceptable standard.

• Approval rights over operational decisions: If investors can veto hiring, spending, or pivots below a high threshold, you will feel this daily.

These are not automatic deal-breakers, but they are worth negotiating even if it delays closing by a week or two.

The Real Question: What Are Your Alternatives?

The most important variable is your situation, not the term itself.

Ask yourself three things:

• How long can you run without this funding? If you have 60 days of runway, the leverage to negotiate is low, and delay is genuinely dangerous.

• Are there other investors at the table? One competing term sheet changes the dynamic completely. Use SheetVenture to identify active investors who match your stage and sector before you are down to one option.

• Will this investor open doors or just write a check? A slightly unfavorable term with a top-tier lead can outperform perfect terms from a passive fund.

If you have runway, alternatives, and time, negotiating harder is almost always the right move. If you have none of those, accepting and moving forward is often the rational decision.

Terms That Should Stop a Round Cold

A few provisions are hard to come back from regardless of circumstances:

• Cumulative dividends: Accrue year over year and inflate the amount investors recoup at exit.

• Drag-along rights with low thresholds: Forces all shareholders to sell if a small percentage agrees, often without founder consent.

• Broad IPO ratchets: Guarantee investors extra shares if the IPO price falls below their entry.

• Personal guarantee clauses: You should not be personally liable for company performance.

These are not "slightly unfavorable." If you see them in a term sheet, get a lawyer who knows VC deals before you sign anything. Read about equity vs. notes to understand how deal structure affects long-term founder outcomes.

The Bottom Line

Slightly unfavorable terms on valuation, board representation, or standard liquidation preferences are usually worth accepting to close a good round with the right investor. Participating preferred, multiple liquidation preferences, or anything that restricts your operational control is worth negotiating even under time pressure.

The deciding factor is always your alternatives. Build optionality before you need it.

SheetVenture helps founders identify active investors matched to their stage and sector, so you enter every negotiation with real alternatives instead of just one term sheet to accept or lose.

Publication Date: