5 Investor Red Flags That Kill Funding Rounds (And How to Fix Them)

Raising capital is one of the most critical (and stressful) parts of building a startup. Founders obsess over pitch decks, metrics, and warm intros

Last Update:

15 Minutes Read

Investor red flags kill more startups than bad products do. 90% of startups don't make it , and many fail because they trigger warnings that make investors walk away.

Poor products don't cause most failed rounds to collapse. They stall because the financial story feels thin, messy, or hard to believe . Investors back businesses they can understand quickly . This piece walks you through five critical investor red flags that derail startup funding and shows you how to fix them before your next pitch.

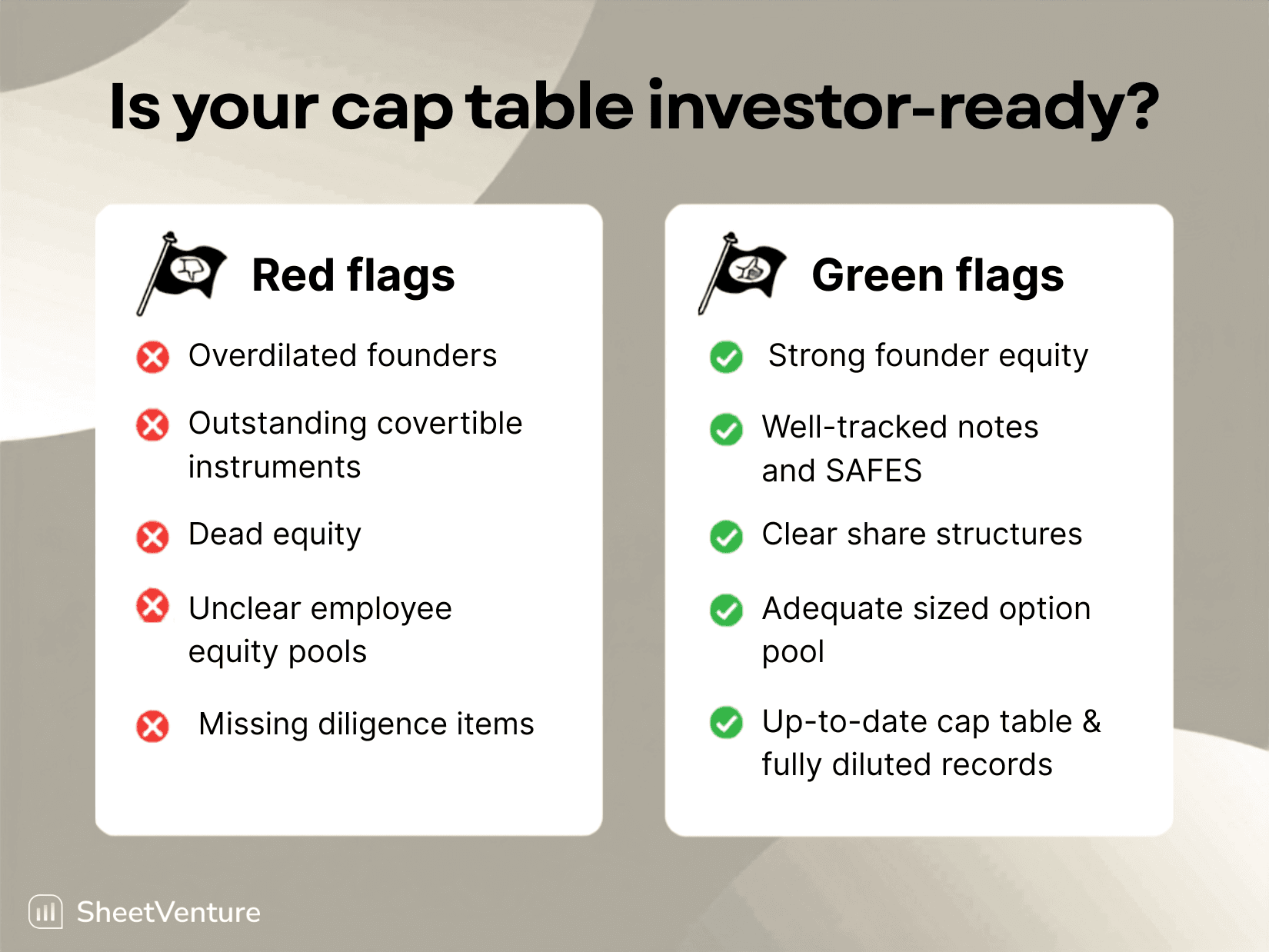

Broken Cap Table and Equity Distribution

Image Source: Cake Equity

A single spreadsheet error on your cap table can cost you an entire funding round. Ownership structure problems appear in one of the first documents investors get into when analyzing startup pitches, and these issues surface during due diligence when it's already too late to fix them easily.

What Makes a Cap Table Uninvestable

A broken cap table means the ownership structure of previous investors creates problems for future investors. The term describes situations where shareholding of those who bring the most value to a company is disproportionately smallercompared to those who contribute nothing [1].

The first problem happens when founders give away too much equity too early. Inexperienced founders often hand over excessive ownership because they don't understand market standards or because they received only one term sheet and had no negotiating power [1]. Companies that face low valuations or operate in small niches with limited international traction sometimes see founders accept investment proposals that take too much equity simply to survive.

Founders should retain a majority in their company after a seed round, ideally after Series A as well [1]. Silicon Valley Bank notes that industry experts expect founders to sell 20-35% of their company during Series A [2]. Subsequent rounds that push ownership too low cause founders to lose influence on the board, and investors question their long-term commitment.

Dead equity creates another uninvestable scenario. This refers to company shares owned by individuals who no longer contribute but still hold stock [1]. The situation happens when a founder leaves after conflict but keeps their equity. Equity should motivate active contributors, not reward people who walked away, at least from an investor's viewpoint [3].

I discussed with a company that raised from both VCs and angel investors and now has 100 investors in their cap table recently. You would need three busses to gather all their investors [1]. Some VCs refuse to invest in companies with more than 20 investors in the cap table [4]. Each additional investor adds weeks to closing, and coordinating that many parties on major decisions becomes impossible.

Effect on Startups Funding Rounds

Cap table errors kill fundraising deals outright. Missing documentation, misrepresented share classes, and unconsolidated investor lists create red flags that surface during due diligence and derail rounds that seemed certain [4].

An Excel cap table claiming a key engineer owns five percent means nothing without executed legal documents backing it up. Every equity grant needs a board resolution, an option agreement, and a signed acceptance from the recipient. Resolving these documentation gaps can take months if recipients have left the company or relationships have soured [4].

Startups on Carta's cap table management platform raised 18.4% more capital in 2024 than in 2023, but they did so on 7.3% fewer total rounds [5]. Investors are getting pickier. Down-rounds become problematic, not only from a PR viewpoint but also affecting employees and investors. Things might get sorted out after a few discussions when we're talking about a 5-10% down-round. But drastic valuation decreases, such as Klarna's 86% drop between 2021 and 2022, make it much more difficult to keep the company afloat [1].

Inaccurate cap tables damage credibility and reputation, eroding investor trust and scaring away other potential investors [3]. Investors who cannot trust you to deliver accurate information through your cap tables cannot trust you to manage millions as capital.

Warning Signs Investors Look For

Investors get into specific patterns that signal deeper problems:

Too many minor shareholders: Cap tables requiring page breaks are red flags. Having lots of investors becomes distracting, which translates into risk. Investors also like to own large parts of the company, and negotiating future ownership stakes with lots of small owners becomes risky [6].

Lopsided founder equity: When two founders have 50/50 ownership and one decides to leave due to conflict but keeps their equity, a motivation problem exists for the remaining founder [1]. Investors prefer distributed equity, though an 80-20 split between co-founders will raise questions [5].

Missing vesting schedules: Almost 70% of investors will walk away viewing the lack of vesting alignment as a red flag [7]. Without reverse vesting or vesting rules among founders, it becomes very difficult to sort out equity when someone leaves.

Unaccounted convertible instruments: SAFEs and convertible notes not reflected in the cap table cause unexpected dilution that damages investor trust [8]. Without careful modeling, large conversions at low valuations can catch everyone off guard.

Impossible scenarios: Shareholder ownership listed as more than 100%, securities granted to non-existent individuals, and instances of negative equity qualify as serious mistakes that aren't logical [3].

Inconsistent documentation: Common issues include investors listed as 'angels' instead of being named, no record of price per share at each relevant event, and SAFEs labeled as convertible loan notes [3].

How to Fix Cap Table Issues Before Pitching

A partial or full buyout might solve the problem if you realize you've given out too much equity to passive angel investors or advisers who no longer bring value [1]. These buyouts happen at a discount from the last round's currently perceived valuation in my experience. Buying out equity from inactive shareholders also serves as a chance for existing and new investors to increase their shareholding.

Create a separate investment vehicle (SPV) through which they represent one legal entity in your company when you have multiple small investors creating complexity. This unites dozens of angel investors into a single entity on your cap table [4]. The second solution, less ideal for managing ownership structure, involves giving power of attorney to one investor to represent the other 99 [1].

Sign a founders agreement as early as possible. This contract governs business relationships and defines how much ownership each founder holds and what happens when any of them leave the company, avoiding future disputes and ensuring fair equity distribution [1].

Clean your cap table before fundraising starts. Every equity grant, option, and convertible instrument should be reflected in one authoritative record [2]. Maintaining organized records demonstrates that your startup can manage financial and legal matters, showcasing attention to detail and commitment to good governance.

Build a healthy habit by starting with ten minutes daily for each equity-related task [3]. Without a clear outline of the company's growth, it becomes difficult for a lawyer or accountant to jump in and reverse-engineer the information. You don't really have a cap table at all if you have a messy cap table that you're not updating. There's no source of truth.

Poor Financial Planning and Cash Flow Management

Financial mismanagement destroys more startups than competitive threats. Since 29% of startups fail because they run out of money, understanding your cash position isn't optional [1]. Yet I've watched countless founders walk into pitch meetings with beautiful decks while their financial foundations crumble beneath them.

Burn Rate Growing Faster Than Revenue

Burn rate reveals how aggressively you operate and how long your startup can survive without running out of money. It shows how well you convert cash into progress. When companies plan for what they'll do with the next funding round rather than plan based on the funding they already have, trouble follows [1]. That next funding round may not happen.

The numbers tell a stark story. 38% of startups fail due to running out of cash or failing to raise capital [9]. Many first-time founders don't factor salaries and benefits into their calculations of future cash burn properly. They often underestimate how many people they will need if they do factor them in [1].

You can make an informed decision on how much needs to be raised to cover the burn rate for long enough to achieve your goals by understanding your unit economics and your cost of growth. Companies should raise enough to last 12-18 months as a general rule [1]. You'll want to bring down the burn rate before drastic, last-minute surgery is required if your unit economics are eroding and there are less than 12 months of runway [1]. It takes five months or more to raise funds typically.

Burn rate reflects strategy, not just expenses. Two startups can have similar revenue, but their burn rate tells different stories completely. One might spend $350K monthly while doubling revenue and hitting product milestones, appearing fundable for Series A. Another burns $70K monthly yet shows flat revenue and no product progress [9]. Investors look at the burn rate to figure out how long the startup can keep going before it will need more money [9].

A high burn rate might mean the company is spending too much without good reason. A balanced burn rate suggests the company is strategic about its spending [9]. You're not investing if burn stays flat forever. You're not learning if burn only rises without efficiency [9]. The surprising result was that under-spending money also increases the chances of a company's failure [10].

Messy or Unreliable Financial Records

Investors rely heavily on the objectivity and integrity of those who prepare financial statements. Any confidence that may have been invested in the reporting system is destroyed when that fiduciary bond is broken and the reliability of financial statements is called into question [3].

Cash versus accrual confusion distorts growth, margins and runway. Revenue gets recorded when cash hits the bank with cash accounting, not when it's earned. Prepaid annual contracts are recognized all at once instead of over the term [5]. Improper expense categorization creates another problem. Everything ends up in 'General & Admin' or 'Contractors.' COGS and OpEx aren't separated, so you can't calculate gross margin with any accuracy [5].

Missing or incomplete documentation compounds these issues. Customer contracts, vendor agreements and cap table records are scattered across email and Slack. You're hunting for PDFs instead of answering strategic questions when diligence starts [5]. No consistent chart of accounts means new accounts get created on the fly whenever someone doesn't know where to book a transaction. Your P&L becomes a junk drawer instead of a decision-making tool over time [5].

Disconnected systems create additional headaches. Billing, payroll and accounting tools don't sync, so your revenue, headcount and cash numbers don't tie together [5]. 40% of survey respondents attributed their lack of confidence in the accuracy of their financial figures to being overwhelmed by so many data sources [3].

Effect on Investor Confidence

Financial statements are very often the only chance that investors are given to assess both an organization's viability and its life expectancy [3]. What else might be wrong in the eyes of the investor if the financial statements cannot be trusted?

The consequences extend way beyond administrative headaches. 69% of respondents believe they or their CEO have made a most important business decision based on out-of-date or incorrect financial data according to one survey [3]. Organizations have paid upwards of $50K to fix reporting mistakes and $25M in enterprise value to address problems that the right bookkeeping and accounting solution could have addressed early on [5].

It's a sign they're being mismanaged when your company's data looks disorganized, incomplete or otherwise questionable, and that's dangerous for every part of your business [5]. Investors will have a difficult time assessing your liquidity or the value of equity [5]. Messy books can delay or derail deals. Cleanup done under the gun can push out close dates, force painful 'haircuts' on metrics like ARR or gross margin, or cause investors to lose confidence and walk away [5].

How to Build Investor-Ready Financial Systems

It's already late to start a major cleanup by the time you're in the market for a raise [5]. Your startup accounting cleanup should be in motion by the middle of Q2 as a rule of thumb if you're targeting a raise in Q4. That timing gives you room to fix issues, produce clean financials and build confidence before investors start digging in [5].

Startups should prioritize building a solid financial infrastructure from day one. This means implementing strong accounting software and establishing clear processes for expense approval and tracking. You'll need to develop regular financial reporting routines and possibly engage professional financial expertise, even if only on a part-time basis [11]. Regular financial reviews and forecasting sessions can help identify potential issues before they become critical problems [11].

Build a rolling 13-week cash forecast for operational control with your 60-month strategic model. The weekly granularity reveals payroll timing and vendor payment schedules that monthly forecasts miss [12]. Your financial model should connect to your CRM, accounting system and operational dashboards. This ensures investor expectations for data consistency and GAAP compliance are met from day one [12].

Weak Market Validation and Customer Traction

Between 34% and 42% of startups fail because there's no market need [14]. Not because the product doesn't work. Not because the team lacks talent. The business built something nobody wants to buy.

Why Market Research Matters to Investors

Market validation refers to the process of verifying that a product or service has demand in the market [15]. Investors place heavy importance on full market research that indicates promising potential at the time they assess which startups to fund [16]. Providing tangible proof that your product fulfills a market need signals that your startup could be a worthwhile investment.

Investors look for opportunities that offer low risks and high returns. Market validation reduces risk perception by showing substantial market demand [15]. A confirmed market need instills confidence among investors, crowdfunders and banks, and increases your chances of securing the funding you just need by a lot [1]. Effective market validation provides credible data that reflects consumer interest. Investors are inclined to support businesses that back their claims with solid evidence [15].

Traction proves that your business model works and strikes a chord with the market for early-stage startup founders [9]. Even the best pitch can fall flat without traction. Investors in 2025 are prioritizing startups that grow in a sustainable way. Showing traction with smart use of resources is more important than scaling quickly [9].

Common Market Validation Mistakes

Validation means more than getting compliments or nods of approval. It means someone changes their behavior because of what you're building [13]. That's a signal if they give you their email, agree to a follow-up call, commit time to try an early version or pay you money. If they say "That's a cool idea" and nothing more, that's not validation. That's politeness [13].

One of the most common pitfalls founders encounter is solution bias, the erroneous belief that the problem lies in the customer not using your solution [14]. This mindset guides you to building solutions without first confirming the existence of a genuine problem. Hearing positive feedback from friends or family isn't validation. These responses often stem from politeness rather than genuine market need [17].

Avoid asking the wrong questions or asking questions the wrong way during the validation process [14]. Craft questions to avoid confirmation bias that confirms preconceived notions. Skipping market research sets you up for a chain reaction of poor decisions [18]. Good market research means digging deep to understand customer pain points through interviews, surveys and competitor analysis while learning about online communities.

Customer Concentration Risks

High customer concentration occurs when any single customer accounts for 20% or more of your revenue [19]. Relying on one customer to keep your startup afloat is too risky. You're going to be in a tough spot financially if that customer churns or downgrades [20].

No single customer should account for more than 50% of your recurring revenue for early-stage SaaS startups making $200K ARR or less [20]. You reduce potential challenges that can arise from their changes in purchasing behavior, financial instability or switching to a competitor by avoiding heavy reliance on a single customer. Putting all of your eggs in one basket could scare off potential investors [20].

The common definition of customer concentration is a customer or group of customers that account for 8% or more of a company's total sales [21]. You spread out risk and avoid being overly reliant on any one client by acquiring a diverse set of customers across different industries or market segments [20].

How to Show Real Market Demand

Direct conversations remain the gold standard for early validation [10]. Target and reach out to at least 10-12 people who fit your ideal customer profile using LinkedIn, industry forums or your existing network [10]. Ask probing questions like "Walk me through the last time you encountered this problem" and "How much time or money does this problem cost you?" Document patterns and look for recurring themes across conversations.

Landing pages offer a low-cost way to test market interest by simulating a real purchase decision. Dropbox confirmed their idea with a simple landing page and explainer video, generating 70,000 signups before building their product [10].

Nothing confirms an idea like customers willing to pay actual money. Early paid pilots represent the strongest possible validation [10]. Paying customers provide strong validation. In early stages though, think about other markers such as signups for waitlists, pre-orders or letters of intent [14]. Investors want to see that you can turn marketing spend into new customers in a predictable way, proving your startup has found a reliable growth engine [22].

Team Dysfunction and Leadership Problems

Image Source: Allied Venture Partners

Leadership problems destroy startups that should succeed. Investors put money into people first, technology second. Team dynamics fracture and even brilliant products can't save the company.

Founder Conflicts That Raise Red Flags

About 65% of high-potential startup failures stem from people problems involving relationships and decision-making [23]. Conflicts over equity distribution concern investors because they strike at the heart of ownership structure. These disagreements arise from varying perceptions of value contribution, future direction, or personal aspirations [24].

Frequent and unresolved disputes among founders erode investor confidence. Investors seek stability and a cohesive team that can weather challenges together [24]. More than 50% of founders are replaced as CEO by the third round of financing, and 73% of these replacements involve firing rather than voluntary departure [23].

Co-founder tension rarely starts with confrontation. It often begins with silence. Meetings get more formal, Slack threads go cold, and suddenly it's not "we" anymore, it's "I" [5]. You start noticing hesitations before decisions and second-guessing in front of the team. You hear about disagreements through third parties. The gap grows and internal factions form within the team, with people gravitating toward one founder over the other [5].

Unclear Roles and Decision-Making

Role confusion turns capable teams into competing factions. Responsibilities overlap or remain undefined and even your best performers start second-guessing themselves [25]. About 50% of employees don't understand their role fully, and unclear roles slow decisions by 25% [25].

Execution slows in startups not because of weak talent, but because role clarity erodes as companies scale [26]. Ownership and decision rights become ambiguous and strong hires hesitate. Decisions escalate and founders get pulled back into execution. Nothing is broken, yet nothing moves cleanly either [26].

Teams with defined accountability are 31% more productive [25]. Roles lack clear ownership and execution doesn't fail loudly, it leaks. Different people fill different gaps, overlap increases, and tension appears [26].

High Employee Turnover Signals

High turnover represents one of the clearest investor red flags. Companies with high turnover rates lose 18% of their workforce annually, compared to the 12% average in industries of all types [3]. Department-specific attrition represents a clear red flag. Turnover concentrates within certain teams while other departments maintain healthy retention and leadership issues are to blame [3].

Toxic culture proves 10.4 times more powerful than compensation in predicting turnover [3]. The 2021 analysis showed that corporate culture and work environment mattered far more than pay [27]. Employees who strongly agreed that their work is challenging, stimulating, and rewarding have a 73% chance of staying five years or more, compared to a 39% chance for those who strongly disagree [28].

How to Strengthen Team Alignment

Every founding team should have a formal agreement defining what happens if someone wants to leave, how decisions get made, what each founder is responsible for, and how disputes are resolved [5]. Frameworks for decision-making help because you know who leads on what and it's easier to disagree and move on [5].

Regular check-ins allow teams to fine-tune and maintain momentum [29]. Use these opportunities to review progress, address roadblocks, and refocus efforts on shared priorities. Encourage transparent communication where ideas, concerns, and feedback flow freely [29]. Everyone feels heard and informed and it builds trust and keeps the team aligned.

Missing Legal Compliance and IP Protection

Legal compliance gaps create immediate deal-breakers that end funding conversations before they start. Around 67% of startups collapse during fundraising, not because of weak pitches, but due to legal red flags uncovered during due diligence [30].

Regulatory Gaps That Scare Investors

Securities regulations are the foundations of investor protection, yet many startups skip requirements. Any time you issue equity or SAFEs, you're selling securities [31]. Startups must file Form D with the SEC and often Blue Sky filings at state level [31]. Even a small $25K SAFE from a family member requires filing [31]. Without proper securities compliance, your entire offering could be illegal and investors can demand their money back [11].

Industry-specific regulations matter just as much. Healthtech startups need therapeutic goods approvals, fintech companies face anti-money laundering obligations, and data-driven businesses must comply with privacy laws [32]. Investors want confidence that your business can operate as it scales [32]. Missing licenses or compliance processes signal operational risk that kills deals.

Weak Intellectual Property Strategy

Startups with IP protection were 10 times more successful in securing seed funding compared to those without [33]. Without solid safeguards, even inventive companies struggle to secure funding [12]. Patent companies raise capital at 93.2% higher valuations than non-patent companies [34]. Startups with IP rights are 4.3 times more likely to land venture capital funding [12].

Ownership disputes destroy value. If your code was written by a freelancer with no signed agreement, or your patent remains in a cofounder's name, you're flagging serious legal issues [30]. Paying a contractor doesn't transfer IP ownership [32]. Without proper assignment agreements from founders, employees and contractors, investors question what they're investing in [32].

Effect on Future Fundraising

IP portfolios affect your knowing how to raise subsequent rounds. Investors assess IP to gage competitive edge [35]. Weak IP reduces valuation or delays deals entirely [36]. Without protection, competitors copy your innovations freely and legal barriers to entry disappear [33].

How to Address Legal Requirements Early

Conduct an IP audit before fundraising starts. Review patent filings, trademark registrations and IP ownership agreements with all contributors [36]. Ensure founders assigned any pre-incorporation intellectual property to the company [37]. File required securities forms and maintain records [31]. Work with startup attorneys who understand both federal and state securities law [11].

Comparison Table

Red Flag | Effect on Funding | Key Statistics | Warning Signs | Solution/Fix |

Broken Cap Table and Equity Distribution | Kills fundraising deals outright. Missing documentation and misrepresented share classes derail rounds during due diligence | Startups on cap table management platforms raised 18.4% more capital in 2024; 70% of investors walk away if vesting is missing; some VCs refuse to invest with more than 20 investors in cap table | Too many minor shareholders; lopsided founder equity (50/50 splits with departed founders); missing vesting schedules; convertible instruments not factored in; ownership exceeding 100%; inconsistent documentation | Buy out passive investors at discount; unite small investors into SPV; sign founder's agreement early; clean cap table before fundraising; maintain daily equity-related task updates |

Poor Financial Planning and Cash Flow Management | 29% of startups fail from running out of money. Messy books delay or derail deals and investors lose confidence | 38% of startups fail due to running out of cash; 69% of CEOs made decisions based on incorrect financial data; organizations paid up to $50K to fix reporting mistakes and $25M in enterprise value for problems | Burn rate growing faster than revenue; cash vs accrual confusion; improper expense categorization; missing documentation; disconnected systems; 40% overwhelmed by too many data sources | Build financial infrastructure from day one; start cleanup by Q2 for Q4 raise; implement rolling 13-week cash forecast; connect financial model to CRM and accounting systems; raise enough for 12-18 months runway |

Weak Market Validation and Customer Traction | Without traction, even best pitches fall flat. Investors prioritize sustainable growth over rapid scaling | 34-42% of startups fail due to no market need; Dropbox generated 70,000 signups before building product; single customer shouldn't exceed 50% of ARR for early-stage startups | Solution bias (building without confirming problem); positive feedback from friends and family only; high customer concentration (20%+ revenue from one customer); asking wrong validation questions | Conduct 10-12 direct customer conversations; create landing pages to test interest; secure early paid pilots; broaden customer base across industries; document recurring themes from customer interviews |

Team Dysfunction and Leadership Problems | 65% of high-potential startup failures stem from people problems; more than 50% of founders replaced as CEO by third round | 73% of CEO replacements are firings not voluntary; 50% of employees don't understand their role; unclear roles slow decisions by 25%; teams with defined accountability are 31% more productive | Unresolved founder conflicts over equity; co-founder tension and silence in meetings; unclear roles and overlapping responsibilities; high turnover (18% vs 12% industry average); department-specific attrition | Create formal founding agreement; establish decision-making frameworks; conduct regular check-ins; encourage transparent communication; define clear role ownership and accountability |

Missing Legal Compliance and IP Protection | 67% of startups collapse during fundraising due to legal red flags in due diligence; weak IP reduces valuation or delays deals | Startups with IP protection 10x more successful in securing seed funding; patent companies raise capital at 93.2% higher valuations; IP-protected startups 4.3x more likely to land VC funding | Missing Form D and Blue Sky filings; lack of industry-specific licenses; IP ownership disputes; no signed contractor agreements; missing patent and trademark registrations | Conduct IP audit before fundraising; ensure all contributors signed IP assignment agreements; file required securities forms (Form D, state filings); work with experienced startup attorneys; transfer pre-incorporation IP to company |

Conclusion

Fixing these five investor red flags requires time and discipline, but each one is within your control. Addressing all of them at once might feel overwhelming, but you don't need perfection before your first pitch. Start with the issues causing the most risk to your funding round, then work through the rest.

Clean your cap table first and tighten your financial systems second. Confirm your market assumptions third. Address team dynamics and legal gaps before investors start digging into due diligence. These fixes will separate your startup from the 67% that collapse under scrutiny once you enter the fundraising market.

Key Takeaways

These five critical investor red flags can derail your funding round before you even get to pitch your product. Here's what every founder needs to know to avoid these deal-killers:

• Clean your cap table before fundraising starts - 70% of investors walk away if vesting is missing, and some VCs refuse companies with more than 20 investors

• Build financial systems early, not during fundraising - 38% of startups fail from running out of cash, and messy books can delay deals by months

• Validate market demand with paying customers, not compliments - 34-42% of startups fail because there's no market need, despite having working products

• Address team dysfunction before it becomes visible to investors - 65% of high-potential startup failures stem from people problems, not product issues

• Secure IP protection and legal compliance from day one - Startups with IP protection are 10x more successful in securing seed funding and raise at 93% higher valuations

The startups that successfully raise capital aren't necessarily those with the best products, they're the ones that eliminate operational red flags before investors start looking. Since 67% of startups collapse during fundraising due to these preventable issues, fixing them systematically gives you a significant competitive advantage in securing investment.

FAQs

Q1. What are the most common red flags that cause investors to reject startup funding requests?

The five critical red flags are broken cap tables, weak financial planning, insufficient market validation, team dysfunction, and missing legal or IP compliance. These operational and structural problems cause 67% of startups to collapse during fundraising, surfacing in due diligence, not because of poor products.

Q2. How does a messy cap table affect my ability to raise funding?

A disorganized cap table can kill your round. Investors walk away from too many small shareholders (20+), missing vesting schedules (70% reject deals without them), lopsided founder splits, or undocumented grants. Clean it up first: consolidate small investors into SPVs and properly document every equity grant.

Q3. What financial metrics do investors scrutinize most closely during due diligence?

Investors focus on burn rate versus revenue growth, cash runway (aim for 12–18 months), accurate accrual-based records, and proper expense categorization. With 38% of startups failing from running out of cash, build a rolling 13-week cash forecast and make your accounting investor-ready a quarter before raising.

Q4. How much customer traction do I need before approaching investors?

Requirements vary by stage, but investors need proof of real demand beyond friendly feedback. Aim for paying customers, run 10–12 customer interviews, and avoid concentration above 20% of revenue (50% for very early startups under $200K ARR). Since 34–42% of startups fail from no market need, validated demand is essential.

Q5. Why is intellectual property protection so important for securing investment?

Startups with IP protection are 10x more successful at securing seed funding and raise at 93.2% higher valuations. Investors need competitive advantages to be legally defensible, with all IP assigned to the company through signed agreements. Missing IP or compliance (like Form D filings) creates risk that can derail rounds.

Published Date

Related articles

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active