Most VCs shorten deadlines or withdraw when founders shop term sheets. See how the fund tier changes the response.

Most VCs respond to term sheet shopping by shortening expiration deadlines, holding terms firm, or withdrawing entirely. Only 15 to 20% of investors improve their offer when founders reveal competing term sheets. The outcome depends on how transparent the founder is, how competitive the deal is, and whether the VC believes the process is genuine or manufactured.

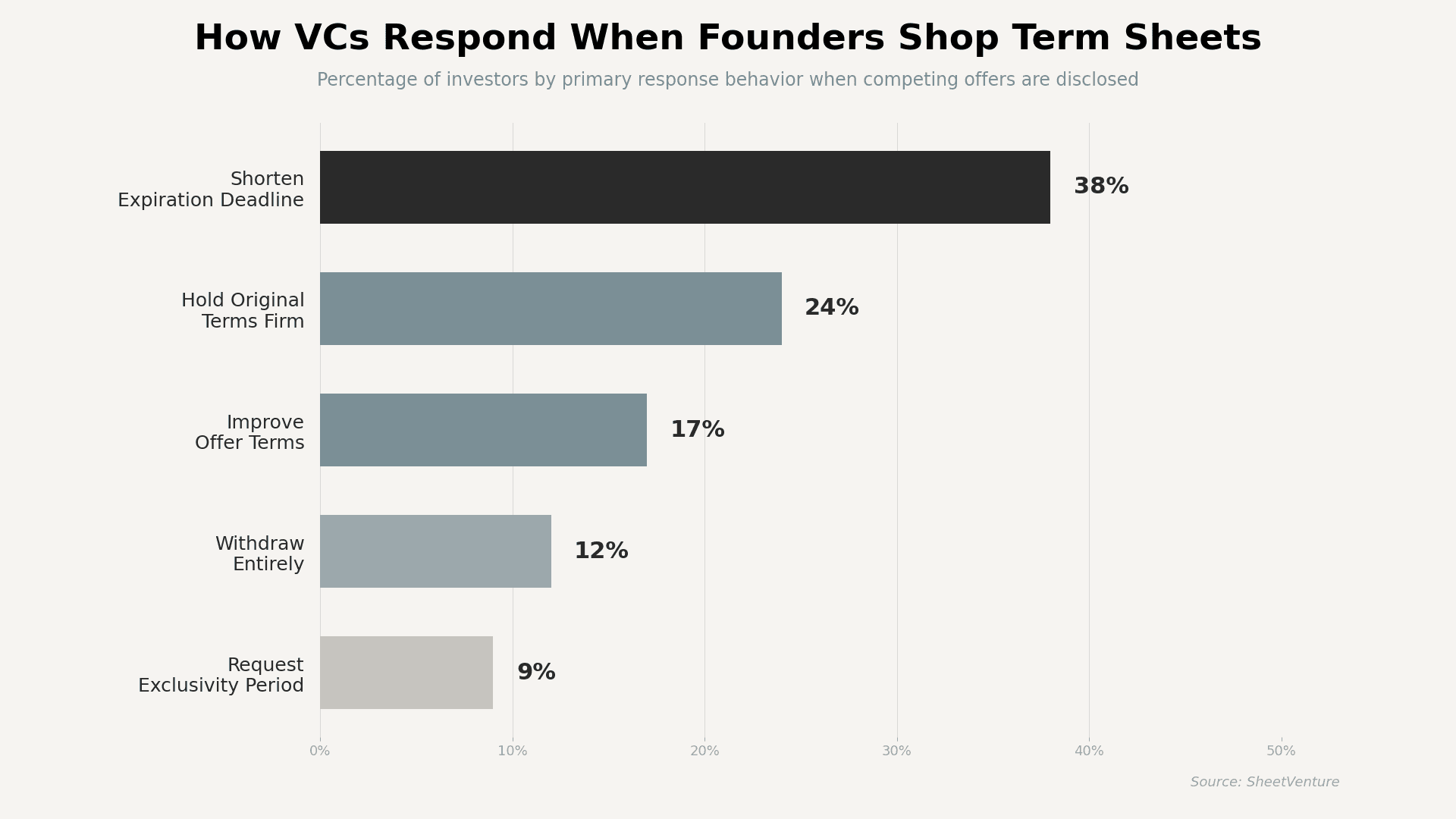

What Happens When VCs Learn About Competing Term Sheets

VCs expect founders to run a competitive process. What they do not tolerate is dishonesty or manipulation. When a founder discloses competing offers, most investors immediately shift into evaluation mode. They assess whether the competition is real, whether the founder is negotiating in good faith, and whether the deal justifies an improved offer.

Common VC reactions:

• Shorten expiration deadlines. 38% of VCs compress timelines to force a faster decision and reduce negotiation leverage.

• Hold original terms firm. 24% refuse to adjust, signaling confidence in their offer and testing founder conviction.

• Improve offer terms. 17% sweeten valuation, board structure, or pro rata rights if the deal is truly competitive.

• Withdraw entirely. 12% pull their offer if they sense the founder is playing VCs against each other insincerely.

• Request exclusivity. 9% ask for a no-shop period to lock the founder into a committed negotiation window.

Understanding how investors pass on deals helps founders anticipate when shopping terms will backfire.

How Does VC Response Change by Fund Tier

Not all VCs react the same way. Fund size, deployment pressure, and deal conviction create different behaviors across the investor landscape.

Fund Tier | Likely Response | Deadline Change | Term Flexibility | Walk Away Risk |

Top Tier (a16z, Sequoia) | Hold terms firm | Shortened to 48 to 72 hours | Very low | High if the process feels forced |

Mid Tier ($200M to $1B AUM) | May improve terms | Compressed to 5 to 7 days | Moderate | Moderate |

Emerging Managers (<$200M) | Often improve terms | May extend slightly | Higher | Low unless burned before |

Solo GPs and Angels | Flexible but cautious | Variable, case by case | High on non-financial terms | Low |

Fund tier shapes negotiation dynamics. Learning how investors delay decisions reveals why some funds need more time before responding to competitive pressure.

What Signals Make VCs Willing to Compete

VCs compete harder when they see:

• Genuine demand. Multiple credible investors engaged simultaneously, not fabricated interest.

• Strong founder transparency. Honest communication about timelines, competing parties, and decision criteria.

• Thesis fit conviction. The deal aligns deeply with the fund's strategy, making a loss feel costly.

• Traction momentum. Metrics that suggest other investors see something validated and growing.

VCs pull back when they see:

• Fabricated urgency. Founders claiming term sheets that do not exist or exaggerating interest levels.

• Auction-style tactics. Pitting investors against each other purely on valuation without relationship signals.

• Delayed transparency. Revealing competing offers only after terms are set, which feels manipulative.

• Mismatched stage or size. The competing term sheet comes from a mismatched investor, signaling the founder is shopping broadly without a strategy.

How Should Founders Manage Multiple Term Sheets

Strategic moves that protect the relationship:

• Disclose early. Tell investors you are running a parallel process from the first meeting. This prevents surprise later.

• Be specific but not aggressive. Share that you have a competing term sheet without naming the fund unless asked directly.

• Set clear timelines. Give all investors the same decision window. Fairness builds trust.

• Evaluate beyond valuation. Board seats, pro rata rights, and follow-on reputation matter as much as price.

• Never bluff. VCs talk to each other. Fabricating term sheets will surface and destroy your credibility permanently.

• Choose a partnership quality. The best term sheet is not always the highest valuation. Operator experience, network access, and follow-on commitment matter more at early stages

Mishandling this process creates signal risk that can shut down your fundraiser entirely.

The Bottom Line

VCs expect competitive processes. They do not expect manipulation. When founders shop term sheets transparently, 17% of investors improve their offers, and most hold firm or compress timelines. When founders fabricate urgency or pit investors against each other dishonestly, 12% withdraw entirely, and reputational damage follows. The VC community is smaller than founders realize. Partners at competing firms share notes, compare deal flow, and remember founders who played games.

The founders who win multi term sheet situations are those who run honest, parallel processes with clear timelines and genuine conviction about their preferred partner.

Ready to run a smarter fundraiser? SheetVenture helps founders identify which investors are actively deploying capital, track competitive deal dynamics, and time outreach so multiple term sheets emerge from a structured, transparent process.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active