Strong Series A companies get rejected at Series B for reasons most founders never see coming. Here's why.

Series B investors pass on strong Series A companies when growth, economics, or team depth fail the scale-stage test. Potential wins rounds at Series A. Proof wins Series B.

Series A is a bet on what you could become. Series B is a judgment on what you already are. Eighteen months of capital, hiring, and growth should have compounded into something durable. When it hasn't, Series B partners pass fast and quietly, often before the second meeting even gets scheduled.

They're looking for a machine now. One that turns $20M into predictable revenue, holds up under real due diligence, and survives a rough quarter without bleeding out. Most Series A winners miss the mark on their first attempt at Series B, and the reasons are consistent, visible early, and almost always fixable with more time.

The Bar Moves Higher

Series A investors ask if you can build it. Series B investors ask if you can scale it. The shift from potential to proof changes everything about the diligence process.

What Series B partners want to see:

• Revenue growing 2.5x to 3x year over year

• Net revenue retention above 120%

• Payback period under 18 months

• Gross margins above 70% for SaaS

• A repeatable go-to-market motion, not founder-led heroics

Miss two of these, and the deal stalls. Miss three, it dies in partner review before a term sheet ever gets drafted.

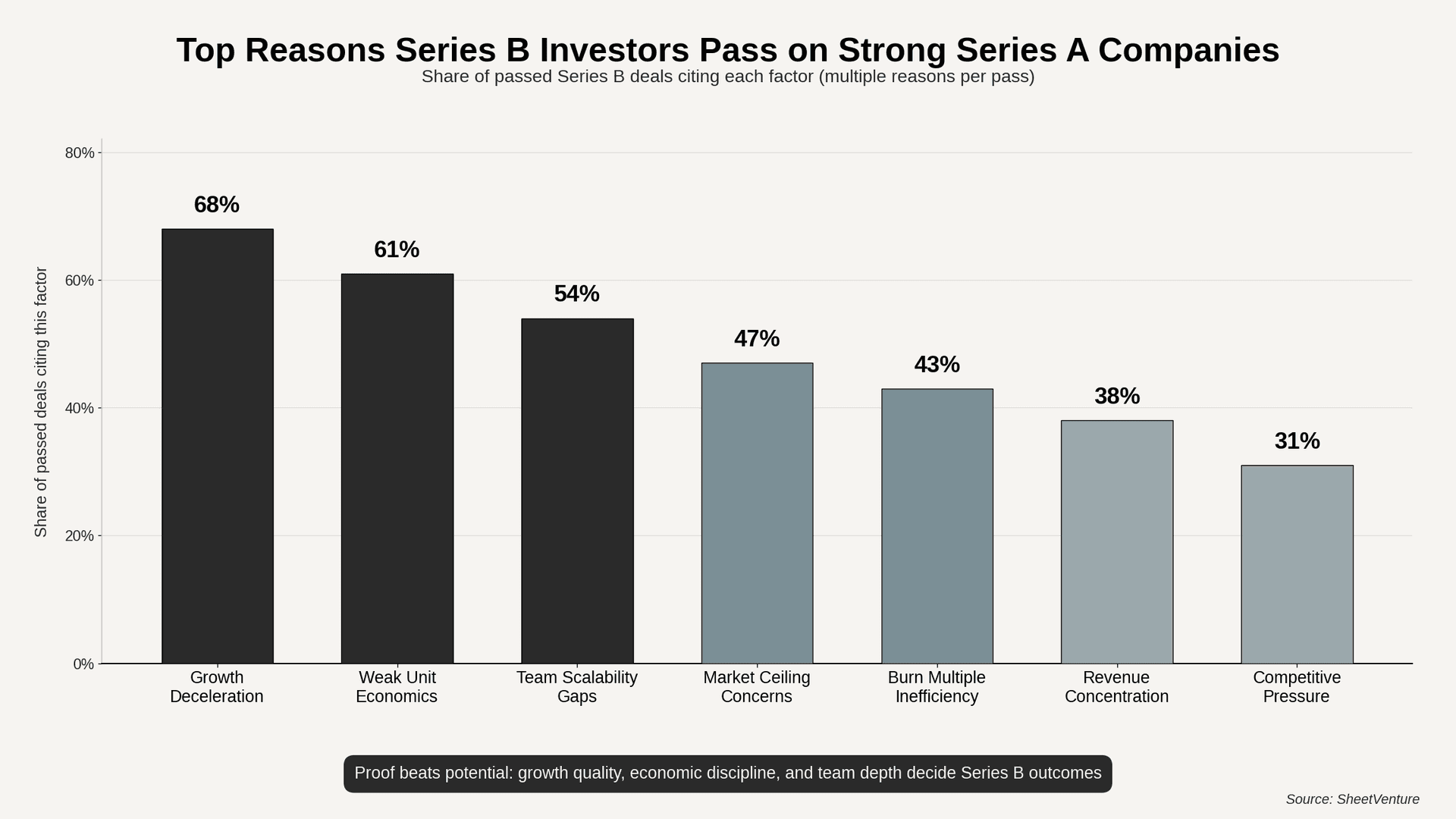

Seven Patterns That Kill Series B Rounds

Pattern recognition across past deals reveals consistent failure modes that founders routinely underestimate:

1. Growth decelerated. The curve bent. Even 80% growth reads weak against a 150% comparable in the same sector during the same quarter.

2. Unit economics slipped. CAC crept up, LTV flattened, payback stretched past 24 months. Scale makes this worse, not better.

3. Concentration risk surfaced. One customer is 30% of ARR. One channel drives 70% of the pipeline. That reads as fragility to a Series B committee.

4. The market ceiling appeared. Bottom-up math exposes a $200M opportunity, not the $10B TAM slide from the Series A deck.

5. The team didn't level up. Founders still run sales, product, and engineering. No VP hires a Series B board that would sign off on.

6. Burn efficiency cracked. A burn multiple above 2.0 means every dollar produced produces less than fifty cents of new ARR.

7. Competitive pressure intensified. A better-funded entrant launched. Differentiation eroded. The moat lost its edge, and the story stopped landing in the partner room.

For the math behind the rejection, read our capital efficiency breakdown.

What Passes and What Fails

The gap between a Series B “yes” and a polite “let's revisit next year” is usually built from small, measurable signals:

Deals that clear the bar:

• Growth is accelerating, not decelerating

• Cohort retention strengthens over time

• Expansion revenue is a real line on the P&L

• The team shows visible operating depth beyond the founders

• One segment is fully owned before the next opens

Deals that stall:

• Vanity metrics hide underlying softness

• Churn is quiet but compounding month over month

• GTM still depends on three founders, not a system

• The roadmap outpaces the actual revenue

• The pitch feels rehearsed, not lived

Our traction quality framework separates real signal from noise that investors learn to ignore.

The Timing Trap

Series A momentum expires. Most companies have 18 to 24 months to make the Series B case before capital markets lose interest and comparable rounds move on to the next cohort. Founders who delay lose leverage. Founders who rush without proof burn relationships they will need later in the round.

The right window opens when growth is steady, economics hold under scrutiny, and the team can credibly absorb a $20M check without operational breakage. Our Series B playbook walks through the full timing framework.

The Bottom Line

Series B investors pass on strong Series A companies because “strong” at one stage rarely equals “ready” at the next. Growth has to compound. Economics have to hold under pressure. The team has to thicken below the founders. The market has to widen, not narrow.

Founders who raise don't just keep executing. They re-qualify their own business against a tougher rubric months before the pitch. Use investor intelligence to identify which Series B funds match your stage, metrics, and sector, then work with SheetVenture to build the outreach pipeline.

SheetVenture helps founders see themselves the way Series B investors see them, long before the meeting that matters most.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active