VCs move faster and compete harder in hot markets but apply much stricter filters when deal flow slows.

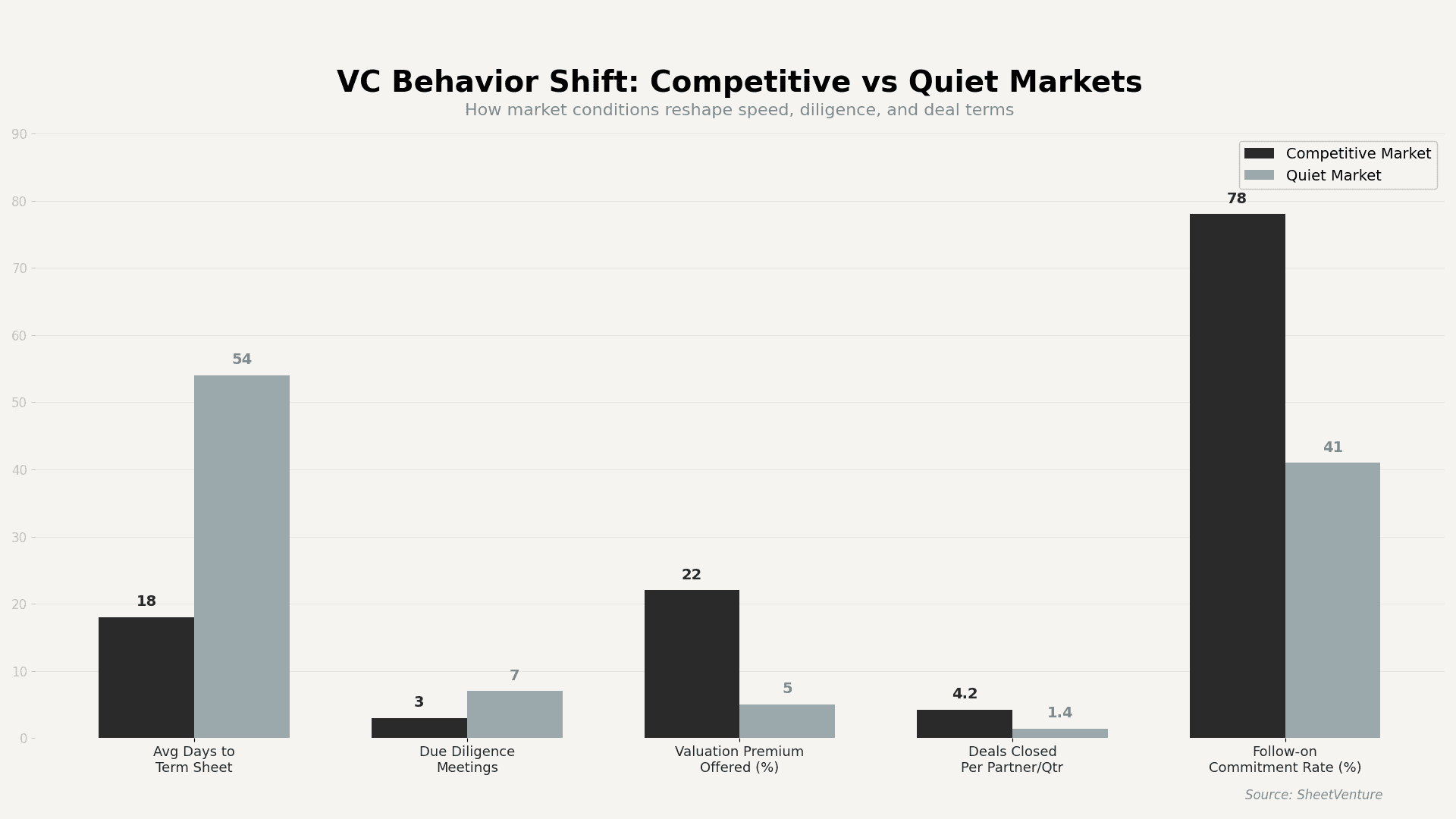

In competitive markets, VCs compress timelines, raise valuations, and fight to win deals because losing a breakout company to a rival fund is the costliest mistake they can make. In quiet markets, that urgency disappears. Capital becomes selective, diligence deepens, and term sheets take weeks instead of days. The same fund that moves in 14 days during a hot cycle may take 60+ days in a downturn.

This shift is not random. It follows a predictable pattern rooted in fund economics, portfolio pressure, and competitive dynamics. Understanding this pattern helps founders time their outreach, calibrate expectations, and choose which investors to approach. Learn how market signals influence whether VCs lean in or pull back.

Why Do VCs Move Faster in Competitive Markets?

When multiple funds chase the same deals, delay equals loss. Competitive markets trigger a set of behaviors designed to reduce the chance of missing winners.

• Fear of missing out (FOMO) accelerates decisions. VCs know that top founders receive 5 to 8 term sheets in hot markets. Waiting means losing.

• Valuation premiums rise to win allocation. Funds offer 15 to 25% higher valuations than they would in normal conditions to secure access.

• Diligence compresses. Standard 6 to 8-week processes shrink to 2 to 3 weeks. Reference checks happen in parallel, not sequentially.

• Partners pre-approve deal ranges. Senior partners delegate authority to move faster without waiting for full partnership votes.

• Follow-on commitment rates increase. VCs lock in pro rata rights early because future access becomes harder to guarantee.

Why Do VCs Become More Selective in Quiet Markets?

When deal flow slows and competition drops, VCs shift from speed to scrutiny. Capital preservation replaces capital deployment as the priority.

• No urgency to commit. Founders have fewer competing offers. VCs can afford to stretch diligence and wait for better terms.

• LPs scrutinize deployed capital. Limited partners pay closer attention during downturns. Funds deploy more cautiously to protect IRR.

• Bar for traction rises. Metrics that would close a deal in a hot market become "interesting but early" in a quiet one.

• Portfolio support demands increase. Existing companies need more attention during downturns, leaving less bandwidth for new investments.

How Do VC Decision Patterns Change by Market Condition?

The table below shows how the same fund behaves differently based on market temperature. These are not different VCs. These are the same partners adjusting to conditions.

Decision Factor | Hot Market | Neutral Market | Quiet Market | Founder Impact |

Time to Term Sheet | 14 to 21 days | 30 to 45 days | 60 to 90+ days | Plan the runway accordingly |

Diligence Meetings | 2 to 3 meetings | 4 to 5 meetings | 6 to 8 meetings | Prepare deeper materials |

Valuation Sensitivity | Low (pay to win) | Moderate | High (negotiate hard) | Set a realistic ask |

Traction Threshold | Narrative + early signal | Clear product market fit | Proven unit economics | Reach milestones earlier |

Competitive Pressure | 5 to 8 funds per deal | 2 to 3 funds per deal | Often 1 or none | Create urgency signals |

Follow on Rate | 75 to 85% | 55 to 65% | 35 to 45% | Negotiate rights early |

Founders raising in quiet markets should expect longer cycles and build their fundraising timeline with at least 50% more buffer than standard advice suggests.

What Triggers the Shift Between Aggression and Selectivity?

Several macro and fund-level signals cause VCs to change behavior.

• IPO window activity. When exits are happening, LPs are happy, and funds deploy aggressively. Closed IPO windows trigger caution.

• Fund lifecycle timing. Year 1 to 2 funds deploy quickly regardless of the market. Year 3 to 4 funds slow down, especially in downturns.

• Interest rate environment. Low rates push capital into venture. High rates make safer returns competitive, reducing VC urgency.

• Peer behavior. VCs watch what other top funds do. When Sequoia or a16z accelerates, the market follows. When they slow, others mirror.

• Deal quality signals. When strong founders cluster in the pipeline, VCs move fast. Thin pipelines trigger patience.

How Should Founders Adjust Their Strategy?

Your outreach strategy should match the current market temperature. Founders who understand investor behavior during different cycles raise more successfully.

• In hot markets: Move fast. Run a compressed process. Use competing interests to drive urgency. Prioritize funds that can be committed quickly.

• In quiet markets: Start earlier. Build relationships before you need capital. Lead with metrics, not narrative. Target funds in early deployment years.

• In any market: Know which investors are actively deploying. A fund in year 4 with 80% capital deployed will not behave like a year 1 fund sitting on fresh capital.

The Bottom Line

VCs are not inherently aggressive or selective. Market conditions dictate behavior. Competitive markets compress timelines by 60 to 70%, inflate valuations by 15 to 25%, and push funds to commit faster with less diligence. Quiet markets reverse all of that. The same partner who writes a term sheet in two weeks during a boom will take two months in a downturn.

Ready to match your outreach to how investors are actually behaving right now? Use SheetVenture to identify which funds are in active deployment and how their pace compares across market conditions.

SheetVenture helps founders track real-time investor activity so outreach lands when funds are deploying, not when they are pulling back.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active