Discover why VCs offer better terms to preempt rounds and how smart founders create competitive dynamics that work.

VCs offer better terms when they believe losing a deal costs more than overpaying for it. Competitive processes force urgency, and investors preempt by improving valuation, reducing dilution, or accelerating timelines when they see real demand from rival firms. The strongest preemptive offers come when founders combine genuine traction with multiple credible investor conversations running in parallel.

Preemption happens when a VC moves before a founder completes their fundraising process. It is not random generosity. It is a calculated response to perceived competition, deal quality, and the fear of missing a breakout company. Understanding what drives this behavior gives founders real leverage, not manufactured pressure.

Why Do VCs Preempt Fundraising Rounds

Investors preempt because waiting carries risk. If a deal enters full competitive mode, price goes up, allocation shrinks, and governance terms tighten. VCs who move early can lock in better economics for their fund.

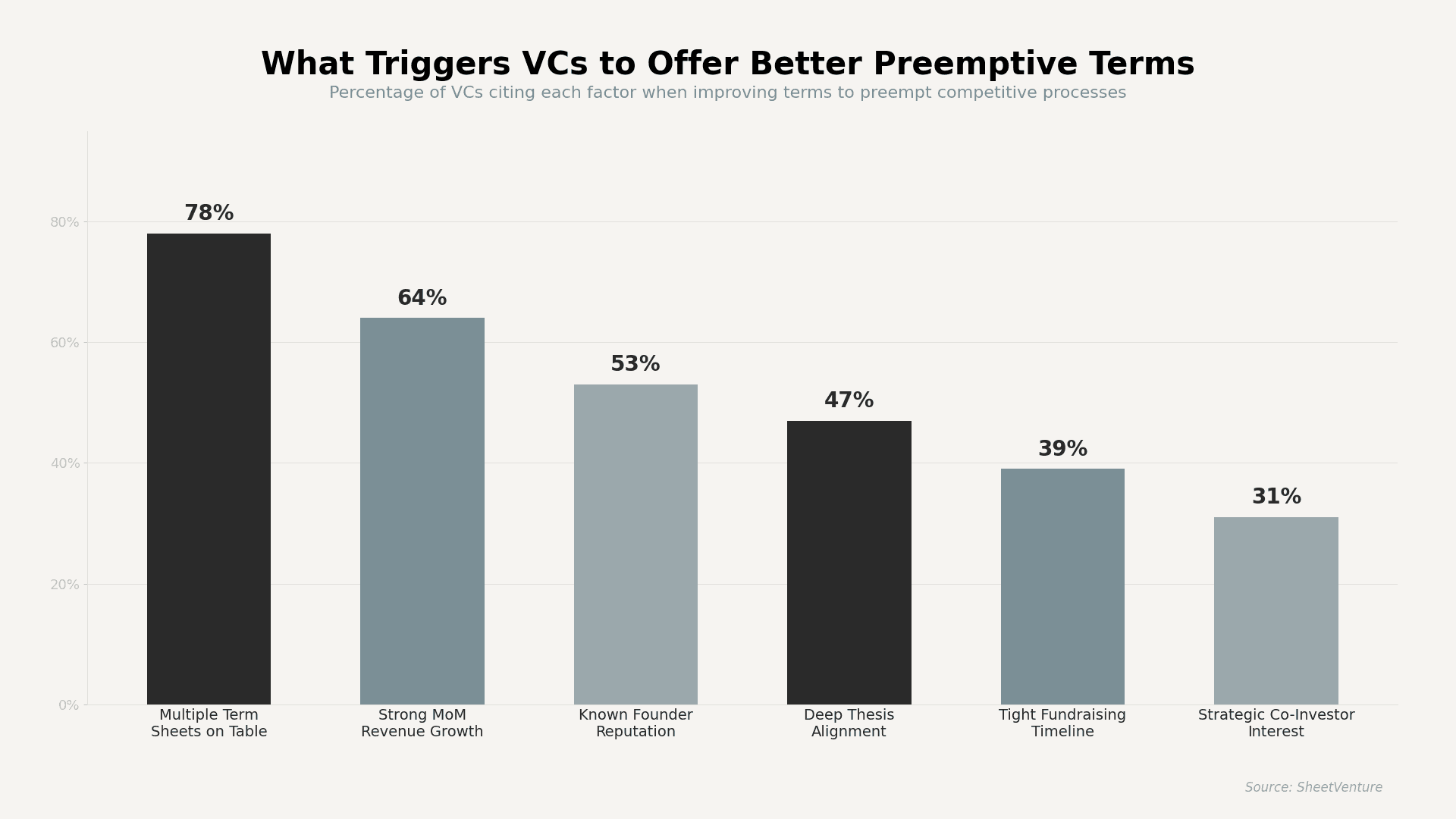

FOMO from co-investor interest: When a VC learns another respected firm is engaging seriously, their internal urgency spikes. Strategic co-investor involvement is one of the fastest preemption triggers.

Traction that speaks louder than the pitch: Strong month-over-month revenue growth or user adoption removes the need to "sell" the deal internally. Numbers do the convincing.

Thesis alignment so deep the partner champions it: When a startup maps directly onto a VC's published investment thesis, the partner has personal conviction and career incentive to move fast.

Founder credibility from prior exits or domain authority: Repeat founders or executives from recognizable companies lower perceived risk, which makes preemption feel safer to the investment committee.

Founders who research VCs before outreach are far more likely to trigger thesis-fit signals that lead to preemptive offers.

What Terms Do VCs Improve in Preemptive Offers

Preemption is not just about higher valuations. VCs adjust multiple deal components to make their offer compelling enough that founders stop the process early.

Term Adjusted | Typical Improvement | When It Happens | Founder Impact |

Valuation Cap / Pre-Money | 15-30% higher than the initial offer | 2+ term sheets competing | Less dilution per dollar raised |

Pro-Rata Rights | Guaranteed follow-on allocation | Strong traction + thesis fit | Signals long-term commitment |

Board Seat Terms | Observer seat instead of a full board seat | The founder has negotiating leverage | More founder control retained |

Closing Timeline | Compressed from 6-8 weeks to 2-3 weeks | VC fears losing to a faster competitor | Faster access to capital |

Anti-Dilution Provisions | Broad-based weighted average vs. full ratchet | Multiple credible offers on the table | Better downside protection for founders |

How Do Founders Create Real Competitive Dynamics

Manufactured urgency backfires. Experienced investors spot it immediately. Real competitive dynamics come from a structured process and genuine interest from multiple parties.

Run a tight, parallel process: Engage 15-25 qualified investors within the same two-week window. Staggered outreach kills momentum and makes it easy for any single VC to wait.

Share progress without fabricating pressure: Mentioning that you are in active conversations with other firms is honest and effective. Claiming term sheets that do not exist is a fast path to burned bridges and what investors call fake urgency.

Let traction create the urgency: Monthly updates showing accelerating metrics naturally generate inbound interest. Investors who see improving numbers between touchpoints feel the pressure of a deal moving without them.

Time your raise around a milestone: Close a major customer, hit a revenue threshold, or launch a product right as you begin outreach. Investors preempt when the trajectory looks inevitable.

Understanding how investors respond to time pressure helps founders calibrate their approach. Pushing too hard risks triggering what investors read as fake urgency, which kills preemptive interest entirely.

What Mistakes Prevent Preemptive Offers

Most founders never receive preemptive offers because they unintentionally remove the conditions that create them.

Approaching investors one at a time instead of in parallel batches eliminates competitive tension.

Sharing too much too early without a clear ask gives VCs permission to wait and watch rather than act.

Targeting investors outside their active thesis or check size range means the deal never reaches a partner with conviction to preempt.

Weak metrics paired with aggressive timelines signal desperation, not demand.

Use investor intelligence tools to identify which firms are actively deploying capital and match your stage, sector, and geography before you start outreach.

The Bottom Line

VCs preempt when the cost of losing a deal outweighs the risk of moving fast. The triggers are consistent: real competitive dynamics, exceptional traction, thesis alignment, and credible founders running structured processes. Better terms are not given. They are earned by creating conditions where multiple investors want in at the same time.

Founders who understand what drives preemption can shape their fundraising process to naturally invite stronger offers without resorting to tactics that erode trust.

SheetVenture helps founders identify which investors are actively deploying, track competitive dynamics across funds, and time outreach so every conversation builds toward the leverage that triggers preemptive offers.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active