When your existing investor passes on your next round, here's exactly what founders must do next.

When an existing investor declines to join your new round, it is not automatically a verdict on your company. Most passes trace back to fund timing, portfolio construction, or a shift in thesis. The right response is to understand the real reason, frame it clearly for new investors, and move forward without losing momentum.

Most founders either overreact or go quiet. They press the investor to reconsider or avoid the topic entirely when pitching new prospects. Treating non-participation as information instead of rejection changes the entire dynamic.

How you explain this moment shapes how new investors read your round. A confident, well-framed answer turns a potential red flag into a non-issue.

Why Existing Investors Pass on Follow-On Rounds

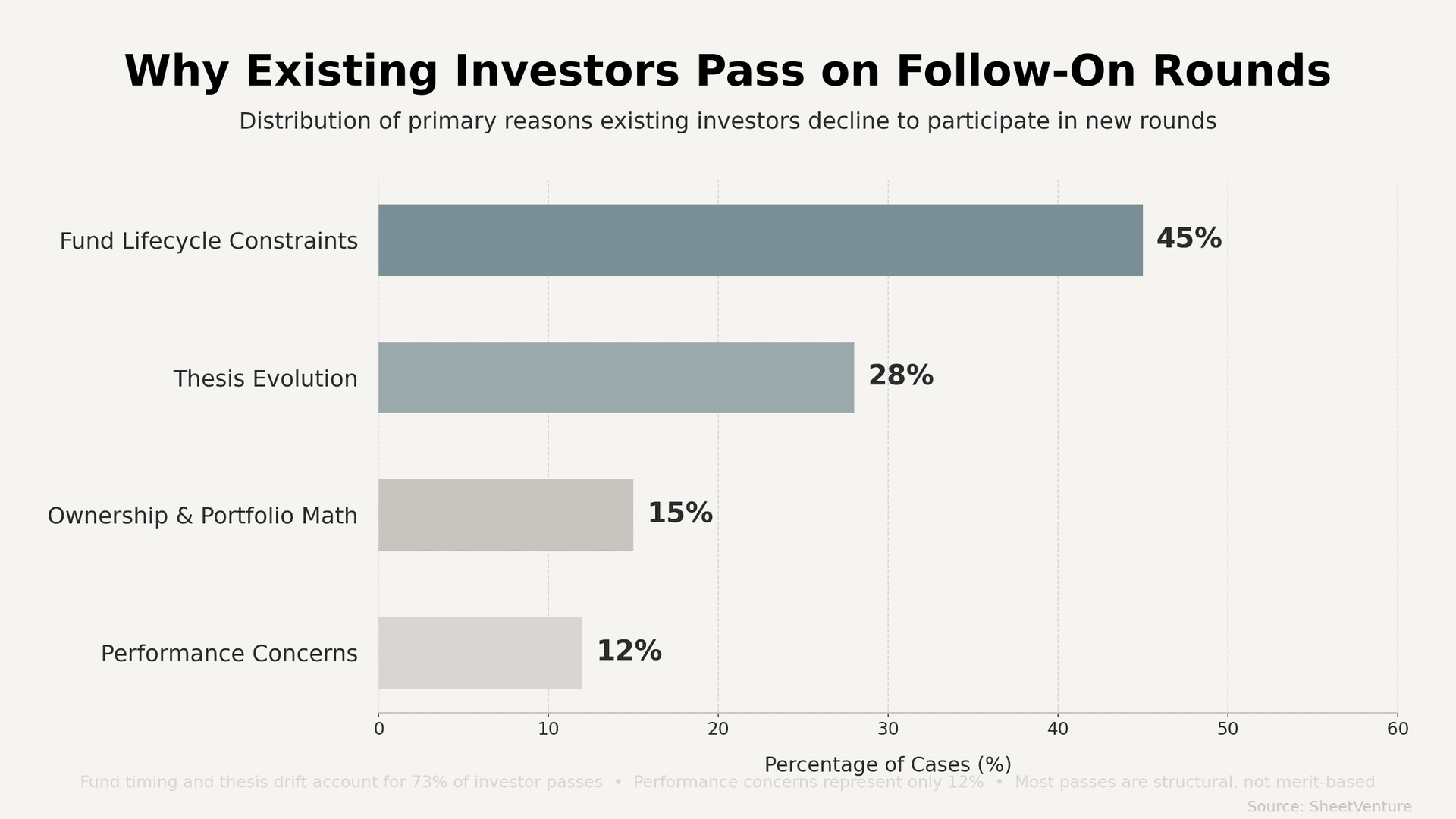

The reasons vary more than founders expect. Fund lifecycle constraints account for the largest share of passes, followed by thesis drift and ownership math. Performance concerns are the minority case, though they get the most anxiety.

• Fund lifecycle: The fund that led your seed may be fully deployed. They have no capital left, regardless of your trajectory.

• Thesis drift: Firms change focus between funds. A firm that backed your seed may have moved toward a different sector by your Series A.

• Ownership math: Some investors will not follow on if their ownership target is already met or if the new valuation changes their return profile.

• Portfolio conflict: If they back a company in your exact space, participating creates a conflict they prefer to avoid.

• Performance hesitation: If the concern is about your numbers, knowing that early changes every pitch you give afterward.

Have the Direct Conversation First

Call your investor before you start pitching new leads. Ask plainly: 'Is this a fund timing issue, a thesis issue, or something about our progress?' Most investors answer honestly when asked directly.

Their answer gives you the language you need with incoming investors. Fund lifecycle explains itself. Thesis drift is easy to contextualize. Performance concerns give you a clear target to address. Going into new investor conversations without a clean answer to 'why isn’t your existing investor in?' is friction you hand yourself.

Managing the Signal With New Investors

New investors will ask about existing investor participation. It is one of the first things they check.

'They have reached the end of their deployment window' lands differently than 'they are passing.' One is structural reality. The other invites skepticism.

What works in pitch conversations:

• Lead with the structural reason if one exists.

• Note if the investor stays on in an advisory or board capacity.

• Mention any signal of interest from their next fund.

• Never hedge or apologize when explaining it.

Understanding how round momentum reads to incoming investors helps you stay ahead of this narrative.

How to Fill the Gap

• Clarify pro-rata rights: Confirm whether your investor is exercising, waiving, or transferring their rights before the round closes.

• Run a real lead search: Find a new lead with the same urgency you used for your original raise.

• Ask for introductions: Even a passing investor can open doors. Ask explicitly.

• Bridge if needed: If runway pressure builds before the round closes, a small bridge from angels keeps momentum intact.

Learning to handle rejections productively applies here. Non-participation is not a closed door unless you treat it like one.

Protect the Relationship

Keep sending updates. Invite the passing investor to observe milestone calls. The investor who skips your A may lead your B if you execute.

Use investor intelligence to find replacement leads who are actively deploying, so you are not targeting funds caught in the same position as your existing investor.

Also, check investor database tools to qualify new leads before spending time on conversations likely to end the same way.

The Bottom Line

When an existing investor passes on your new round, understand the real reason before assuming the worst. Fund timing, thesis drift, and ownership math drive most of these decisions. Address it directly, frame it clearly for new prospects, protect the relationship, and move fast to replace the capital. The way you handle this moment says more about your fundraising maturity than the pass itself.

SheetVenture helps founders confirm which investors are in active deployment windows, so a single investor’s pass does not stall a raise when replacement capital is available right now.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active