Most founders accept bad convertible note terms. Here is exactly what to negotiate, reject, or walk away from.

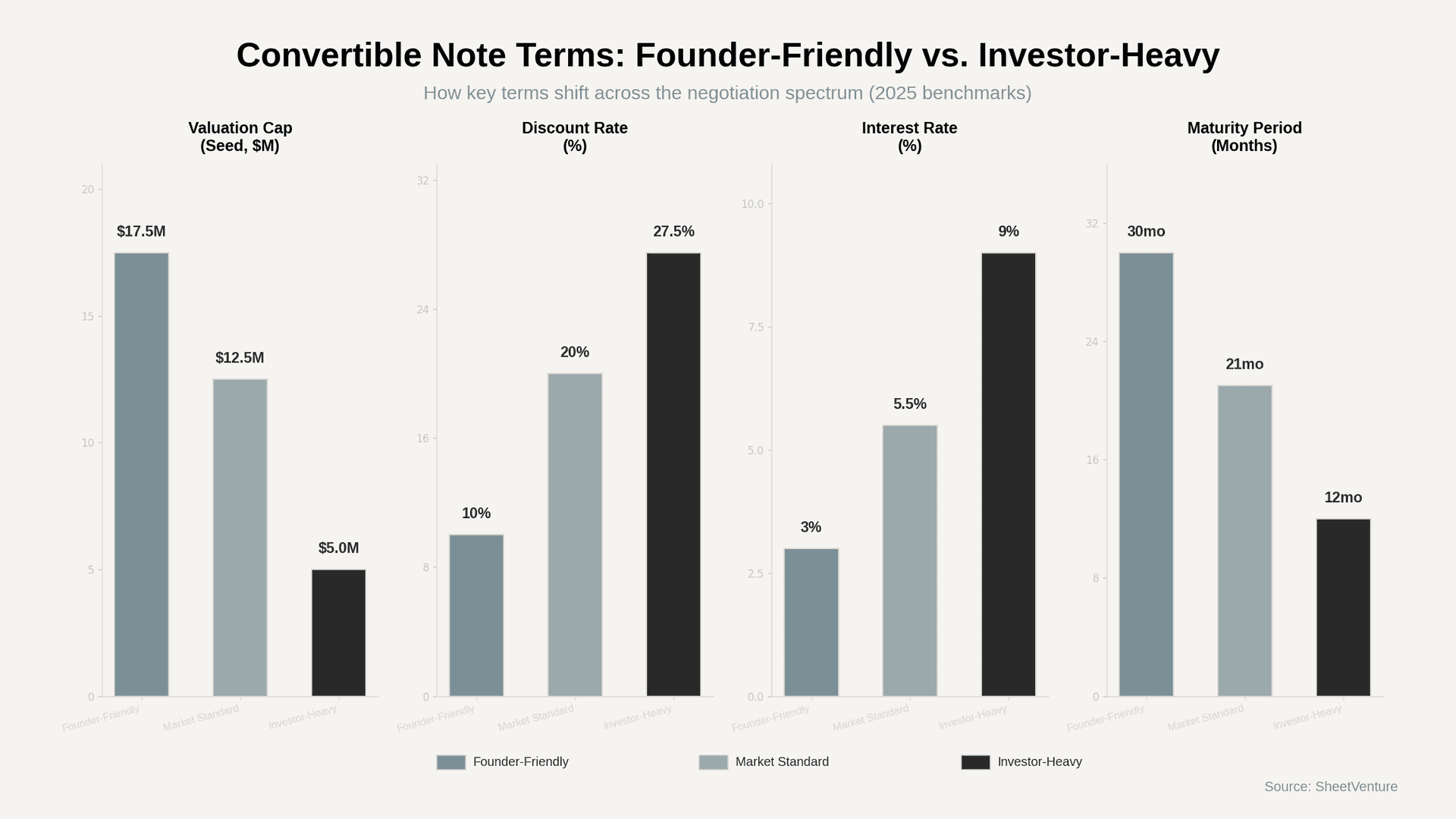

Most convertible note terms are negotiable, and founders who benchmark against market standards hold real leverage. A 20% discount rate, $10M-$15M seed-stage cap, and 18-24 month maturity are standard in 2025. Anything significantly worse deserves pushback or a walk-away.

Receiving a convertible note with aggressive terms does not mean you accept, reject, or panic. It means you evaluate. Founders who understand what a standard looks like can separate genuine red flags from normal investor positioning. The difference between a founder-friendly and investor-heavy note can mean 15-25% more dilution by Series A.

The first move is always comparison. Pull the specific numbers from the offer and measure them against current benchmarks before responding to anything.

How to Spot Unfavorable Terms

Not every tough-sounding clause is predatory. Some terms signal standard negotiation. Others signal a deal you should leave on the table.

• No valuation cap. This is the most dangerous term a founder can accept. Without a cap, the investor converts at whatever price the next round sets, minus their discount. Your dilution becomes unlimited.

• Valuation cap under $6M at seed. Market standard sits between $10M and $15M. A cap at $4M-$6M hands the investor significantly more equity than comparable deals justify.

• Discount rate above 25%. The 20% discount has been standard for over a decade. Anything beyond 25% stacks dilution, especially combined with a low cap.

• Interest rate exceeding 8%. Most notes carry 5-6% simple interest. Rates above 8%, especially with compounding, add meaningful dilution at conversion that founders rarely calculate upfront.

• Maturity under 12 months. Standard maturity runs 18-24 months. Short maturity creates pressure and gives the investor leverage to demand cash repayment or renegotiate from strength.

• Personal guarantees or IP collateral. Walk away. These belong in bank lending, not venture instruments.

• Board seats or veto rights embedded in a note. Convertible notes exist to avoid priced-round governance complexity. If an investor wants board control before pricing, the terms are misaligned.

What Founders Should Do Next

Identifying unfavorable terms is half the work. Acting on that knowledge requires a specific sequence.

• Benchmark first, respond second. Pull data from comparable seed deals in your sector. Share those benchmarks with the investor as your opening position. Saying "market standard for seed-stage SaaS is a $12M cap with 20% discount" carries more weight than "this feels aggressive."

• Negotiate the cap before anything else. Valuation cap drives the most dilution of any single term. If you can only move one number, move this one. Founders often negotiate discount rates when the cap matters far more to ownership at conversion.

• Trade terms, do not just reject them. Offer pro-rata rights in exchange for a higher cap. Extend maturity in exchange for a slightly higher discount. Investors respect founders who negotiate structurally rather than emotionally.

• Get startup counsel to review before signing. A startup attorney costs $2,000-$5,000 for a note review. That investment prevents six-figure dilution mistakes. Use standard documents like YC SAFE or NVCA templates as your baseline, so every deviation requires investor justification. Understanding equity decisions early prevents compounding errors later.

• Know your walk-away triggers. If the investor insists on cash repayment rights at maturity, personal guarantees, or a cap more than 50% below market, the relationship will only get harder. Bad early terms compound through every subsequent financing.

When Walking Away Is the Right Move

Not every deal deserves negotiation. If three or more terms fall in the investor-heavy range, the investor is likely not aligned with founder-friendly practices. Founders who accept predatory terms to avoid losing one investor often find that those terms scare away better investors in the next round. A clean cap table signals discipline. A messy one signals desperation.

Use SheetVenture's investor database to identify investors whose confidence signals match founder-friendly track records before your outreach begins.

The Bottom Line

Convertible note terms are not take-it-or-leave-it. Founders who benchmark against current market data, negotiate the cap first, trade terms strategically, and know when to walk away consistently close better deals. The standard remains a $10M-$15M cap, 20% discount, 5-6% interest, and 18-24 month maturity. Anything significantly outside those ranges deserves scrutiny. Your leverage is knowing the numbers. Use it before you sign.

SheetVenture helps founders benchmark investor terms against real market data so every negotiation starts from a position of knowledge, not guesswork.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active