Most founders email the wrong partner at VC firms. Learn the exact signals that reveal who will respond.

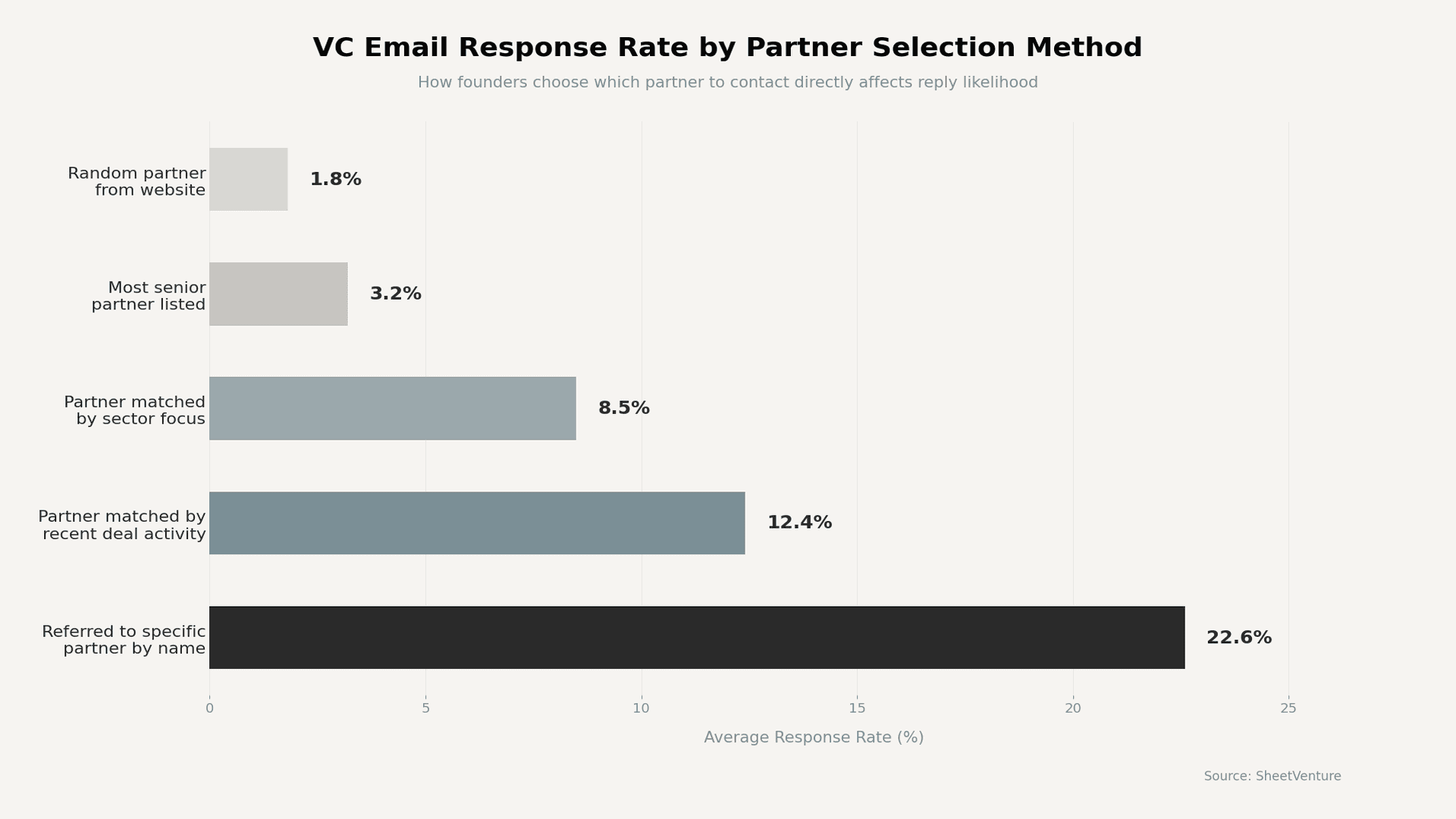

Founders should contact the partner whose recent investment activity, sector focus, and stage preference most closely match their startup. Emailing a random partner from the firm’s website produces a 1-3% response rate. Targeting the right partner based on deal history and thesis alignment increases that to 8-12%.

The difference between a reply and silence often comes down to which name you put in the “To” field.

Why Partner Selection Matters More Than Firm Selection

Most founders spend weeks building a target list of firms but minutes choosing which partner to email. That priority is backwards. Inside every VC firm, individual partners operate with distinct mandates, sector interests, and deal preferences. Two partners at the same fund can have entirely different reactions to the same pitch.

Key reasons partner selection changes outcomes:

• Partners champion deals internally. If the wrong partner receives your email, it rarely gets forwarded to the right one.

• Each partner manages a pipeline of 200-400 inbound emails monthly. Relevance is the only filter that works.

• A partner who recently led a deal in your sector is 3-4x more likely to respond than one focused on a different vertical.

• Associates can forward, but partners decide. Direct contact with the decision maker shortens the path to a meeting.

Understanding investment thesis alignment is the foundation of smart partner selection.

What Signals Reveal the Right Partner to Contact

Five data points separate effective partner targeting from guesswork. Founders who check all five before sending an email see measurably higher response rates.

Signal | Where to Find It | What It Tells You | Priority Level |

Recent deals in your sector | Portfolio pages, Crunchbase, press releases | Active interest and existing thesis conviction | Critical |

Stage preference match | Fund announcements, partner interviews, and deal size patterns | Whether they write checks at your round size | Critical |

Board seats held | LinkedIn, portfolio company filings | Bandwidth for new deals vs. portfolio management load | High |

Content and speaking topics | Blog posts, podcast appearances, Twitter/X threads | Current intellectual interests and thesis evolution | Medium |

Mutual connections | LinkedIn, shared investors, accelerator alumni networks | Warm intro, potential, and social proof leverage | High |

Recent deal activity is the strongest signal. A partner who closed a deal in your vertical within the last 6 months has already done the market homework and is primed to evaluate similar opportunities.

How Do You Research Partner Activity Before Reaching Out

Effective partner research takes 10-15 minutes per firm when using the right sources. The goal is not a complete biography. It is a clear match signal between the partner’s recent behavior and your startup’s profile.

Research steps that produce actionable targeting data:

• Check portfolio pages first. Look for deals closed in the last 12–18 months that share your sector, stage, or business model. Filter out partners focused entirely on the growth stage if you are pre-seed.

• Read their content. Partners who write about your market are signaling active interest. A recent blog post or podcast appearance about your vertical is a strong opening reference.

• Scan LinkedIn activity. Posts, shares, and comments reveal current focus. A partner celebrating a portfolio company in your space is more receptive than one posting about an unrelated thesis area.

Use an investor database to cross-reference deal activity, check sizes, and sector tags across multiple partners at the same firm.

Common Mistakes Founders Make When Choosing a Partner

Targeting errors waste outreach volume and burn potential relationships. The most common mistakes follow a predictable pattern.

• Defaulting to the managing partner. Senior partners have the fullest calendars and the most filters. Unless your sector is their personal focus, junior partners or sector leads are often faster paths to a meeting.

• Emailing multiple partners at the same firm. This signals mass outreach and immediately reduces credibility. Pick one partner per firm based on fit, not volume.

• Ignoring deal recency. A partner who invested in fintech three years ago may have shifted focus. Recent activity within 6-12 months is a reliable indicator.

• Skipping the associate path. At larger firms, associates screen inbound. Identifying the associate who covers your sector can sometimes be more effective than cold emailing a partner directly.

Learn how investors filter emails before responding to understand why precision matters more than volume.

When Should You Contact Someone Other Than a Partner

Not every outreach attempt should target a partner directly. Certain firm structures and situations make alternative entry points more effective.

• Large firms (50+ portfolio companies). Associates and principals run sector coverage. They are incentivized to surface strong deals and often respond faster.

• Platform or scout programs. Some funds run scout networks or platform teams that evaluate early opportunities before routing to partners.

• Venture partners or advisors. Part-time partners often have lighter inboxes and direct influence on deal flow. They are underused entry points at many firms.

Explore how partner meetings work internally to understand who actually champions deals past the first conversation.

The Bottom Line

The right partner at the right firm responds. The wrong partner at the right firm is deleted. Founders who invest 10-15 minutes researching recent deal activity, sector focus, and stage alignment per partner see 3-4x higher response rates than those who email the first name on a website. Partner selection is not a detail. It is the strategy.

SheetVenture helps founders identify which partner at every firm matches their sector, stage, and deal size so outreach reaches the person most likely to respond.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active