Most founders schedule too few investor meetings weekly. Data shows 10–15 weekly meetings close rounds 40–60% faster.

The optimal cadence is 10–15 investor meetings per week during a focused 3–4 week sprint. Founders who maintain this pace close rounds 40–60% faster than those who spread meetings across months, because concentrated scheduling creates competitive urgency among investors and keeps deal momentum alive.

That number surprises most first-time founders. They assume two or three meetings a week is reasonable, and it is comfortable. But comfort kills momentum. When investors sense they are the only ones evaluating your deal, the urgency to act disappears. A concentrated cadence forces parallel conversations, overlapping diligence timelines, and the kind of social proof that makes partners push deals through partner meetings faster.

How Many Investor Meetings Per Week Close Rounds Fastest?

Data across seed and Series A rounds shows a clear relationship between weekly meeting volume and close speed:

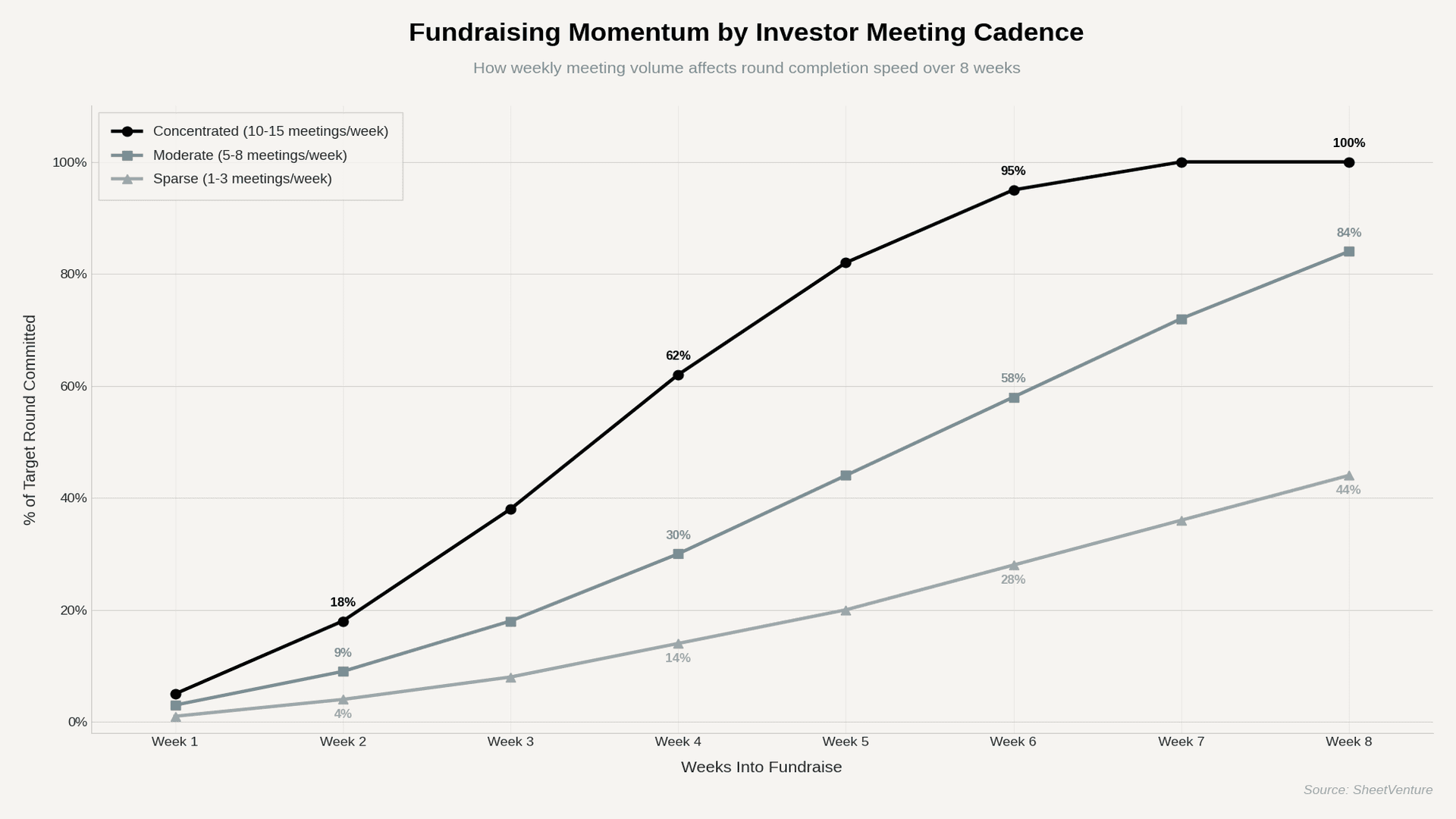

1–3 meetings/week: Round takes 5–8+ months. Investors lose context between conversations. Momentum never builds.

5–8 meetings/week: Moderate pace. Round closes in 3–5 months. Some competitive tension, but often not enough to force decisions.

10–15 meetings/week: Sweet spot. Round closes in 4–8 weeks. Parallel conversations create urgency. Investors hear about you from other investors.

15+ meetings/week: Diminishing returns. Quality of preparation drops. Follow-up becomes unmanageable unless you have a dedicated fundraising operator.

The 10–15 range works because it creates natural scarcity signals. When three investors hear your name in the same week from different sources, pattern recognition kicks in.

What Meeting Schedule Pattern Builds Real Momentum?

Not all cadences are equal, even at the same volume. The structure of your weekly schedule matters as much as the count.

Cluster meetings in 2–3 day blocks. This protects your product work and creates energy from back-to-back conversations.

Batch by investor tier. Start with your middle-tier targets to refine your pitch, then schedule top-tier firms in weeks 2–3.

Reserve 1–2 follow-up slots per day. Second meetings with interested investors should happen within 48–72 hours of the first.

Never schedule first meetings on Fridays. Decision-making energy is lowest at the end of the week.

How investors react to the pace of your fundraising process tells you whether your cadence is working.

How Does Meeting Cadence Affect Fundraising Outcomes?

The table below shows how different weekly meeting volumes correlate with actual fundraising timelines and conversion rates across early-stage rounds.

Weekly Meetings | Avg. Days to Close | Investor Response Rate | 2nd Meeting Conversion | Term Sheet Probability |

1–3 meetings | 150–240 days | 8–12% | 15–20% | 3–5% |

5–8 meetings | 90–150 days | 15–22% | 25–35% | 8–12% |

10–15 meetings | 30–60 days | 22–30% | 35–50% | 15–25% |

15+ meetings | 25–45 days | 18–25% | 30–40% | 12–18% |

Notice the 15+ bracket. Speed keeps improving, but conversion rates actually dip. That is the preparation penalty. When you run too many first meetings, your pitch quality suffers, and follow-up delays start costing you deals you would have closed at a sustainable pace.

When Should Founders Speed Up or Slow Down Meeting Cadence?

Speed up when:

• Multiple investors request second meetings in the same week.

• A lead investor signals strong interest, and you need alternatives to create leverage.

• Your metrics just hit a new milestone that strengthens the narrative.

Slow down when:

• Feedback from the first 10–15 meetings reveals your pitch needs reworking.

• Response rates drop below 10% consistently, which means targeting is off.

• You are burning through top-tier prospects before the pitch is sharp.

Building a properly segmented pitch list before you start prevents burning your best contacts during the learning phase.

What Cadence Mistakes Kill Fundraising Momentum?

Dripping meetings over months. Investors talk to each other. If nobody else is moving on your deal in the same window, there is no urgency to act.

Front-loading all meetings in week one. You need runway for follow-ups and second meetings. A first meeting without a fast follow-up is a wasted meeting.

Ignoring investor signals between meetings. How investors interpret your round momentum depends heavily on what happens between meetings, not just during them.

Treating all meetings as equal. A warm intro meeting and a cold outreach meeting require different preparation and have different conversion expectations.

The Bottom Line

The founders who close rounds fastest run 10–15 investor meetings per week in concentrated 3–4 week sprints. This cadence creates competitive tension, keeps your deal top of mind across multiple firms simultaneously, and shortens the decision window from months to weeks. Below that pace, momentum never forms. Above it, preparation quality drops, and you start losing deals you should have won.

Structure beats volume. Cluster your meetings, tier your targets, and protect follow-up slots. Fundraising is a campaign, not a slow drip of conversations.

SheetVenture helps founders build targeted investor lists with real-time activity data so every meeting slot goes to an investor who is actually deploying capital right now.

Last Update: