VCs bring external advisors into diligence when five specific gaps appear. Learn what each advisor type signals and how founders should respond to compress the timeline.

VCs bring external advisors into due diligence when five conditions appear: the technology requires domain expertise the partnership lacks, the regulatory environment creates liability the firm cannot assess independently, a customer reference pattern produces inconsistent signals, the competitive landscape requires third-party mapping, and the founding team's technical claims cannot be verified without specialist validation.

External advisors are not a sign of interest. They are a sign of a specific knowledge gap the firm decided was worth closing before committing capital.

Why External Advisor Involvement Changes the Process

When a VC brings in an external advisor, every other part of the evaluation is already resolved. The advisor's verdict becomes the last open question between the firm and a term sheet.

Understanding how long VC due diligence usually takes explains why advisor involvement extends timelines without changing overall conviction and why founders who misread the delay as cooling interest disengage at exactly the wrong moment.

The 5 Conditions That Trigger External Advisor Involvement

Deep technical complexity: The advisor confirms the technology does what the founder claims before the firm bets on it.

Regulatory and compliance risk: Healthcare, fintech, and defense startups operate in environments where a single regulatory misread can make the business model illegal.

Inconsistent customer references: When one reference contradicts traction claims, firms bring in a domain expert to interview the customer base independently.

Competitive landscape uncertainty: Advisors with active industry relationships surface competitive dynamics no database captures in real time.

Technical team validation: A technical advisor reviews the codebase and architecture to confirm the team can execute what the pitch describes.

What Each Advisor Type Signals About Where the Deal Stands

Advisor Type Brought In | What It Signals | What the Founder Should Do |

|---|---|---|

Technical domain expert | Firm has conviction on market, needs tech validation | Prepare codebase and architecture documentation immediately |

Regulatory or legal specialist | Business model risk is the last open question | Provide compliance documentation proactively before asked |

Customer reference interviewer | Traction claims produced inconsistent signals | Offer additional references beyond those already provided |

Competitive landscape researcher | Firm cannot internally map the market | Share proprietary competitive intelligence not publicly available |

Financial model auditor | Unit economics require independent verification | Walk through every assumption before advisor reviews independently |

The pattern: Each advisor type signals a specific unresolved question. Founders who identify which advisor was brought in and respond with the exact evidence compress the remaining diligence timeline significantly.

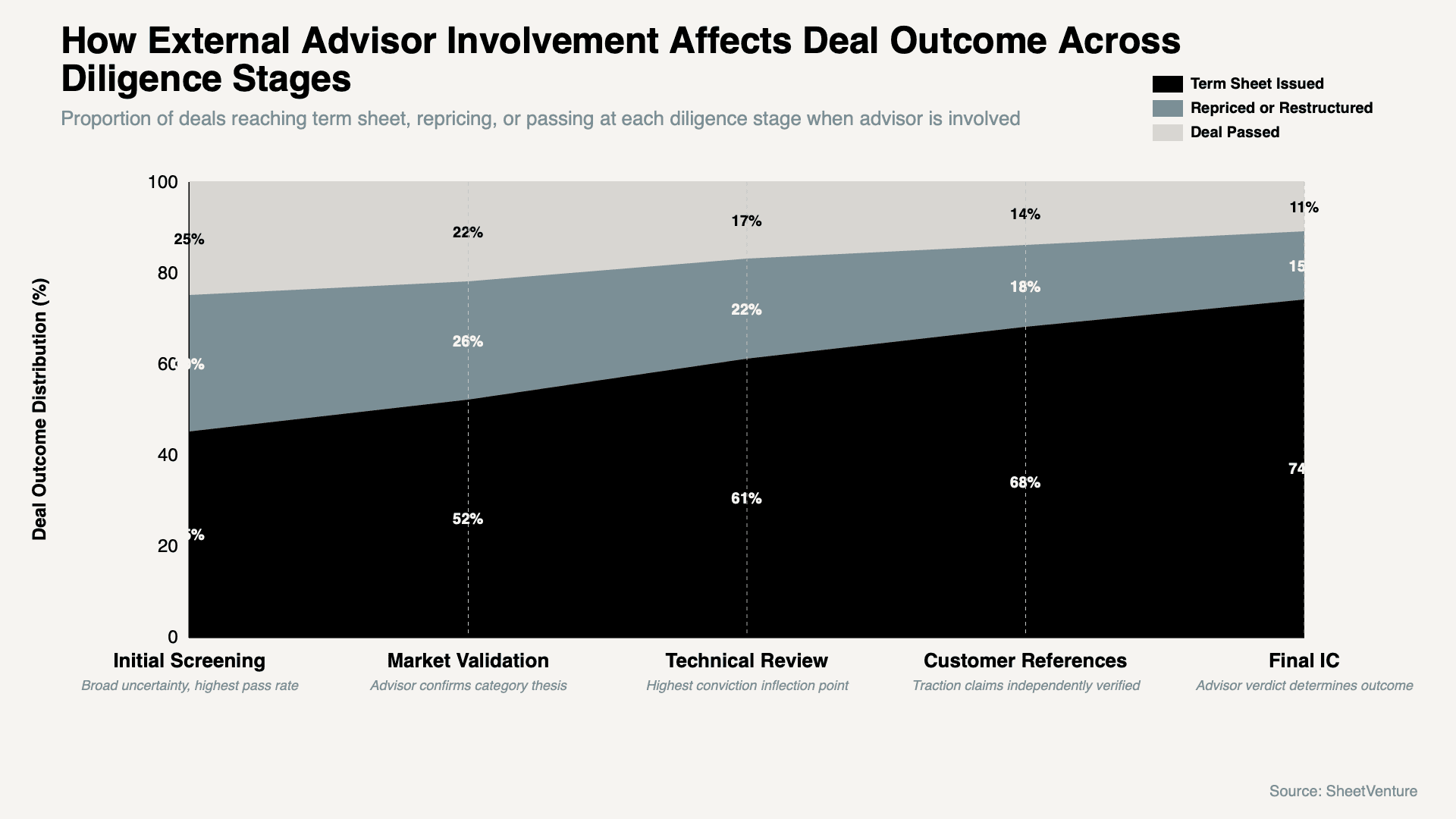

How External Advisor Involvement Affects Deal Outcome Across Diligence Stages

Term sheet probability rises from 45% at initial screening to 74% at final IC, confirming that advisor involvement moves deals toward close when founders respond correctly to each validation request.

Use investor intelligence to research which advisors specific firms use so documentation is prepared in the format those advisors prefer before the request arrives.

How Founders Should Respond When an Advisor Is Brought In

Ask which specific question the advisor is answering so preparation addresses the exact gap

Provide documentation before the advisor requests it so the review begins from transparency

Facilitate advisor access to customers and codebase directly rather than routing interactions through the partner

The principle: The advisor was brought in because the firm wants to say yes and cannot yet. Transparency accelerates it. Defensiveness kills it.

Learn how investors assess execution risk at early stages and how external advisors convert execution risk from a subjective judgment into a documented assessment.

The Bottom Line

VCs bring external advisors into due diligence when technical complexity, regulatory risk, inconsistent customer signals, competitive uncertainty, or technical team claims create a knowledge gap the partnership cannot close internally. Founders who identify which gap triggered the request and respond with precise documentation compress the remaining timeline.

SheetVenture helps founders identify which firms regularly use external advisors so due diligence preparation accounts for the extended timeline and the specific documentation those advisors require.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active