Liquidation preferences, board seats, and anti-dilution clauses shape founder outcomes more than valuation. Learn five terms that matter most long-term.

The terms that most affect founder outcomes long-term are liquidation preferences, pro-rata rights, protective provisions, board composition, and anti-dilution clauses. These determine how much founders actually receive at exit, how much control they retain during the company's life, and whether they survive a down round with equity and decision-making authority intact.

Valuation gets the attention. These terms do the damage.

Why Founders Optimize for the Wrong Number

A founder who negotiates a $20M valuation but accepts a 2x participating preferred liquidation preference has traded long-term exit economics for a number that looks good on a press release. In most acquisitions below $100M, the liquidation preference structure determines founder payout more directly than the valuation cap ever did.

Understanding how much equity to give investors gives founders the foundation for evaluating not just percentage ownership but how that ownership behaves under different exit scenarios.

The 5 Terms That Shape Long-Term Founder Outcomes

Liquidation preference: A 1x non-participating preferred is standard and founder-friendly. A 2x participating preferred means investors get twice their money back before founders see anything, then participate again in remaining proceeds. In sub-optimal exits this structure can reduce founder payout to near zero.

Pro-rata rights: The right for investors to maintain ownership in future rounds. Broad pro-rata rights across a large early investor base can crowd out new strategic investors at later stages and create cap table complexity that institutional investors specifically avoid.

Protective provisions: Veto rights over specific decisions including fundraising, acquisitions, and executive hiring. Expanded protective provisions that require investor approval for operational decisions transfer effective control without appearing on any org chart.

Board composition: Who sits on the board determines who approves CEO compensation, strategic pivots, and founder termination. A board structured as two investors and one independent from seed creates a default investor majority before Series A closes.

Anti-dilution provisions: Full ratchet anti-dilution in a down round can wipe out founder equity entirely by resetting investor share prices to the new lower valuation, triggering conversion ratios that transfer ownership faster than any dilution from new shares.

Term Impact by Exit Scenario

Term | Impact in Strong Exit | Impact in Moderate Exit | Impact in Down Round |

|---|---|---|---|

1x non-participating preferred | Neutral, converts to common | Neutral | Founder retains upside |

2x participating preferred | Reduces founder share 15 to 30% | Reduces founder share 40 to 60% | Founder receives near zero |

Broad pro-rata rights | Limits new investor flexibility | Complicates Series B terms | Blocks strategic capital |

Expanded protective provisions | Slows acquisition approval | Requires sign-off on pivots | Investors block restructuring |

Investor board majority | Board approves exit terms | Board controls strategic options | Board can replace founder |

Full ratchet anti-dilution | Minimal impact | Significant dilution | Near-total equity transfer |

The pattern: Terms that appear minor in a strong exit produce catastrophic outcomes in moderate or down round scenarios. Founders who negotiate exclusively for the strong exit case accept terms that destroy outcomes in every other scenario.

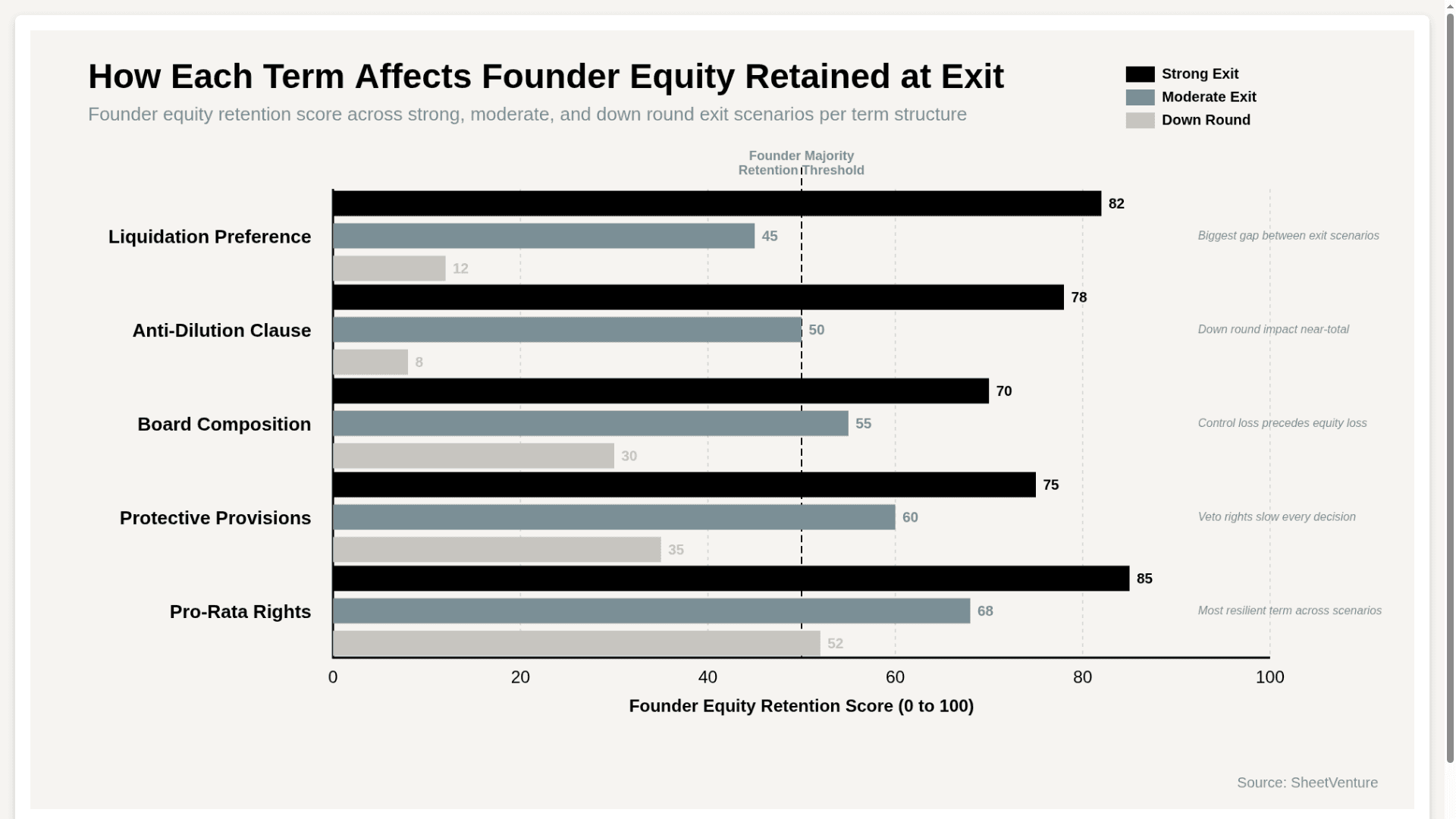

How Each Term Affects Founder Equity at Exit Across Three Scenarios

The chart shows liquidation preference and anti-dilution producing the steepest drops between strong and down round scenarios, confirming that the two terms founders negotiate least aggressively produce the most severe outcomes when the exit does not match the optimistic projection the term sheet was written against.

What Founders Should Do Before Signing

Request 1x non-participating preferred as the default and treat any deviation as a significant economic concession requiring a valuation increase to compensate

Cap pro-rata rights at major investors only and exclude small check writers whose participation creates cap table complexity without strategic value

Negotiate board composition before close rather than accepting default structures

Review protective provisions line by line focused on which operational decisions require investor approval that should not

Learn what a SAFE note is and how it works and how early stage instrument choice determines which terms become negotiable at the priced round stage.

The Bottom Line

Liquidation preferences, anti-dilution provisions, board composition, protective provisions, and pro-rata rights operate invisibly in strong exit scenarios and destructively in every other scenario. Founders who negotiate valuation hard and accept standard terms elsewhere are optimizing for the outcome they want while accepting the terms that govern every outcome they are likely to face.

Valuation is the headline. Terms are the fine print that actually pays out.

SheetVenture helps founders research which investors typically push for founder-friendly terms so every negotiation starts with the right counterparty, not just the highest valuation offer.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active