Discover when raising Series A becomes too early after seed and what ARR thresholds investors demand in 2026.

Raising Series A within 12 months of seed is too early in 2026. Most investors now expect 18 to 28 months of post-seed operating history, $2M+ ARR, and 3x year-over-year growth before engaging seriously.

The Series A bar has quietly reset. What qualified as a clean Series A in 2021, roughly $1M ARR with 2x growth, is now a seed extension conversation. Founders who were raised in the ZIRP era cleared rounds in 18 months on thin traction, and that benchmark still lingers in founder chats.

The 2026 reality looks different. Carta data shows the median seed-to-Series A timeline stretched from 18 months in 2021 to roughly 28 months today. Only 15 to 18 percent of seed companies raise a priced Series A within 24 months, nearly half the graduation rate of the 2018 to 2020 cohorts.

How long after seed should you raise Series A?

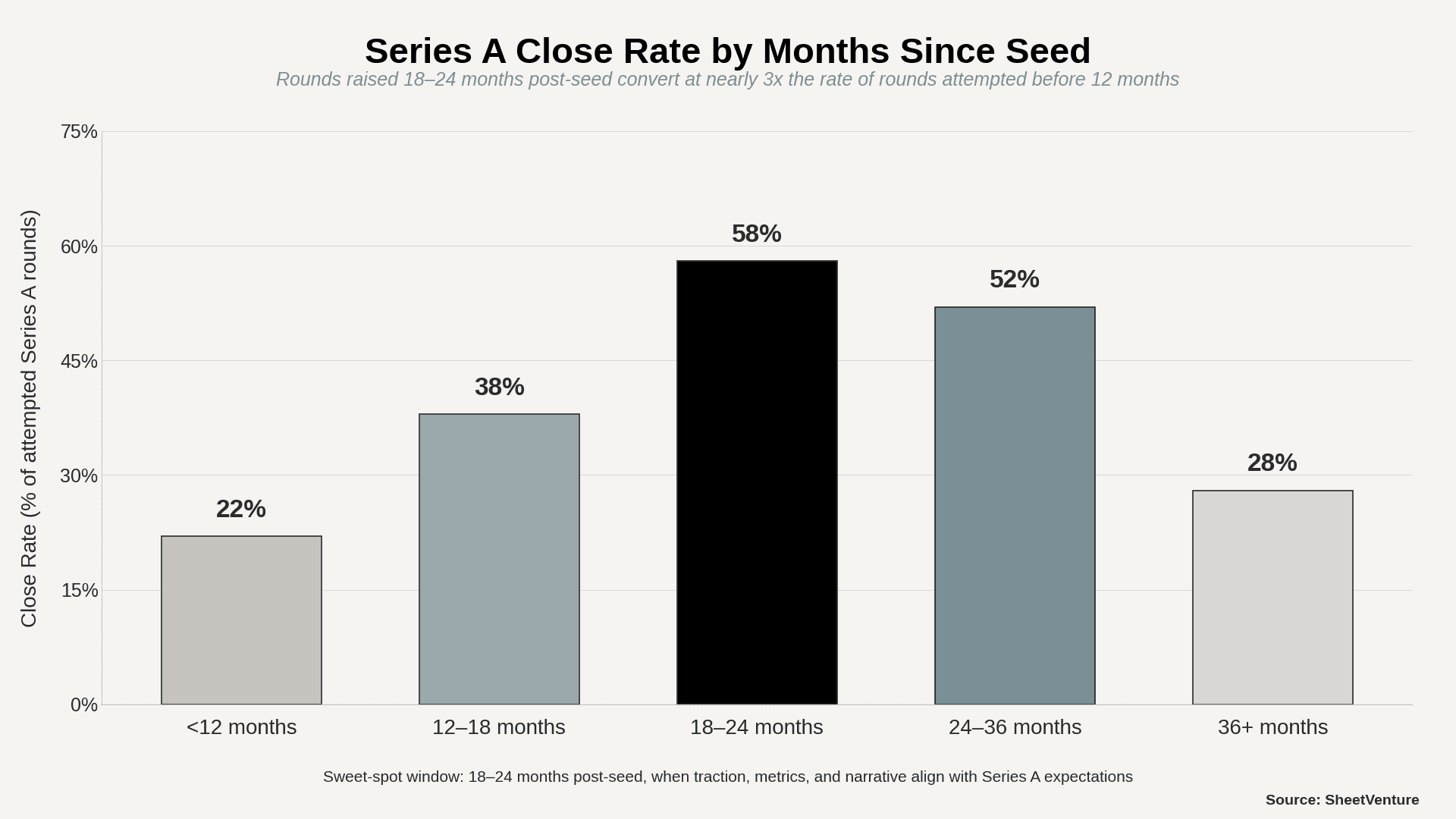

The honest answer depends on traction, not calendar time. Most successful Series A rounds close between 18 and 30 months post-seed, with 24 months as the modal point.

Timeline benchmarks by cohort:

• Under 12 months: early warning zone for most sectors.

• 12 to 18 months: possible only with breakout metrics.

• 18 to 24 months: the new sweet spot for priced rounds.

• 24 to 30 months: normalized, no stigma attached.

• 30+ months: requires a strong narrative to avoid staleness.

Consumer and deeptech founders often need longer runways. AI-category founders with credentialed teams sometimes close faster, though those rounds are outliers, not the template.

What ARR is needed for Series A in 2026?

The current bar by sector:

• B2B SaaS: $2M to $3M ARR growing 3x year-over-year.

• Consumer subscription: $3M to $5M ARR with 25%+ day-30 retention.

• Marketplace: $10M+ GMV with 100%+ cohort retention.

• Applied AI: higher than traditional SaaS, since revenue is easier to generate, but production stickiness is harder to prove

Beyond raw revenue, investors scrutinize quality metrics hard. Net revenue retention above 110 percent, gross retention above 85 percent, CAC payback under 18 months, and a burn multiple below 2x have become table stakes. Top-quartile rounds clear at 120%+ NRR. This is where progress pace signals separate the fundable from the premature.

What signals mean your Series A is too early?

A round is likely premature if three or more apply:

• ARR below sector threshold with no 90-day path to hit it.

• Founders personally closing every deal, no rep-led motion.

• Fewer than three retention cohorts or six months of predictable revenue.

• Over 25 percent of ARR is concentrated in one customer.

• Monthly growth under 15 percent, flat or declining trend.

• Net revenue retention below 100 percent or visible logo churn.

• Gross margin under 60 percent with no cost-structure fix.

• Runway under nine months, pressuring the round at any price.

Each is solvable in 6 to 12 months of focused execution. Together, they signal to come back later to any serious lead. Read too early signs before triggering a process.

Seed extension vs Series A: which is right?

Seed extensions now represent roughly a third of all seed-stage rounds. In the first half of 2025, more capital flowed into extensions than into first-time seeds on Carta, a first for the platform.

Take the extension when:

• ARR is under $1.5M.

• You have fewer than three quarters of post-revenue data.

• Existing investors will lead flat-to-up.

• You want to preserve valuation optionality.

Raise the price A when:

• ARR is $2M+ growing 3x with rep-led sales.

• NRR sits above 110 percent with strong logo retention.

• You have six months of pipeline visibility.

• The $10M ARR runway is clearly mapped.

Extensions stay light: SAFE notes, 5 to 15 percent dilution, no board seat. A priced Series A round locks in 20 to 25 percent dilution and a valuation floor you must beat at Series B. Down-round risk roughly triples when founders raise too soon, Series B graduation rates halve, and recovery often takes 12 to 18 months. Cap-table cleanup, re-pricing, and narrative reset absorb the cycle founders thought they were shortening.

The Bottom Line

Under 12 months post-seed is almost always too early. The 18 to 28-month window has become the realistic range for priced Series A rounds in 2026. The real gate is not time but traction: $2M+ ARR, 3x growth, 110%+ NRR, and a repeatable GTM motion.

Speed is not a signal of strength. Raising when weak locks in a valuation you may never grow past. Raising when strong compounds optionality.

Most founders who rush lose more than they gain. The ones who wait raise cleaner rounds at better terms with the right lead.

SheetVenture pinpoints which investor intelligence is writing Series A checks right now, so timing decisions match real deployment data, not outdated benchmarks.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active