When a seed-stage investor wants board control, it changes everything. Here is what founders must do to protect themselves.

If an investor wants board control at the seed stage, push back. Seed rounds rarely justify majority board seats for investors, and agreeing to them early limits your decision-making authority for every raise that follows.

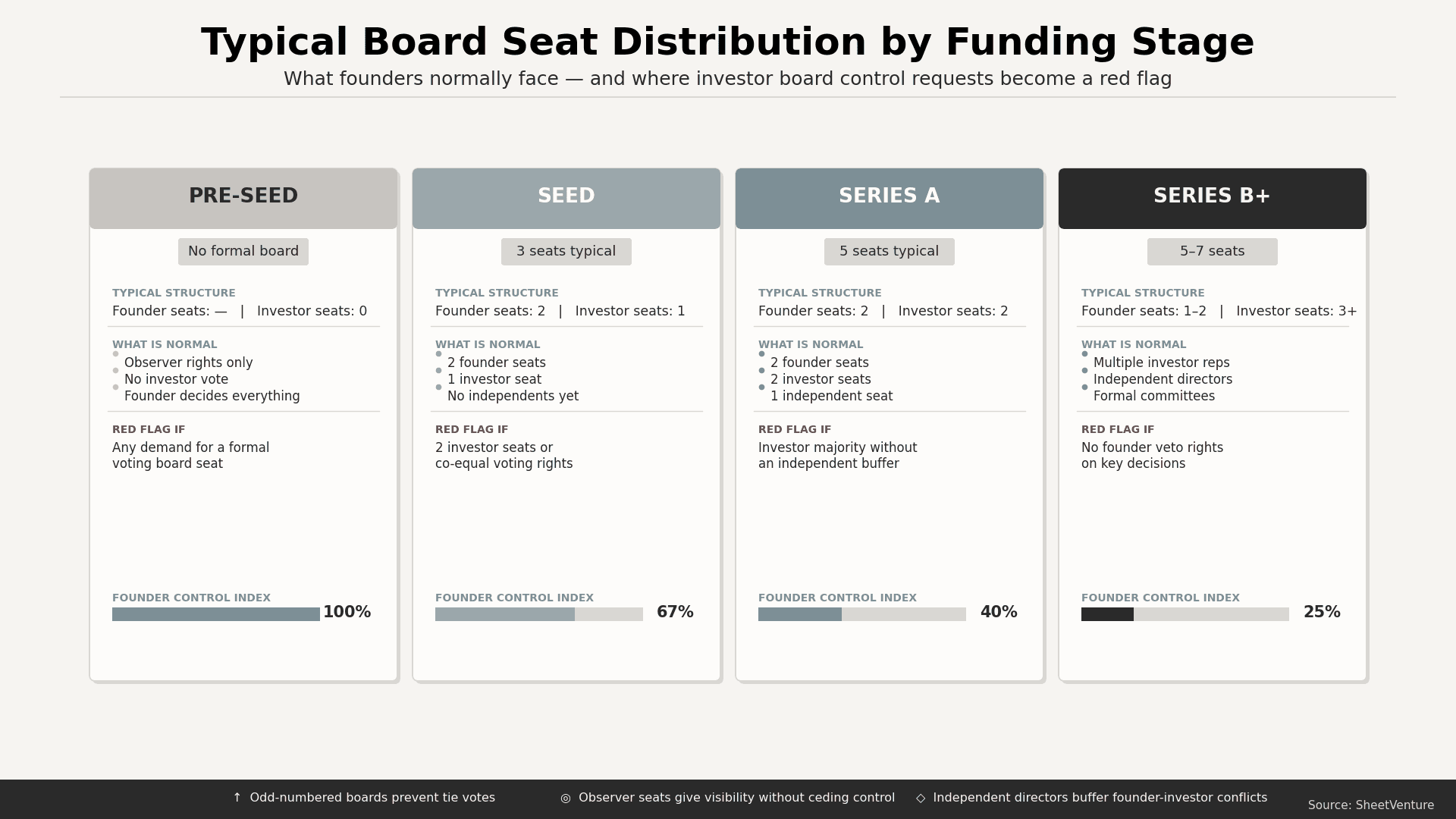

Most founders who give up board control before product-market fit end up answering to investors before they have answered to the market. Understanding what is normal at seed gives you the leverage to negotiate or walk away.

What Board Control Actually Means

Board control is not a title or formality. It is operational power.

An investor with board control can:

• Block a pivot you believe is necessary.

• Override a hire or fire decision.

• Delay or accelerate an exit on their timeline.

• Veto follow-on financing terms you want to accept.

At the seed stage, you are still figuring out the product. Handing veto power to someone who holds a financial interest but not an operational context is a risk that founders underestimate until it is too late.

What Is Normal at the Seed Stage

Most seed-stage companies operate with a three-person board: two founder seats and one investor or independent seat. Some early rounds have no formal board at all, just observer rights for investors.

Anything beyond one investor seat at seed is unusual. Two investor seats that equal or exceed founder seats are a red flag worth addressing before you sign anything.

Use SheetVenture to research how the investor has structured boards in previous seed investments before you ever sit down to negotiate.

Why Investors Ask for Board Control

Not every demand for board control is predatory. Some investors ask because:

• They have backed founders who burned capital without accountability.

• Their fund structure requires board representation for LP reporting.

• They apply later-stage terms to early rounds out of habit.

Understanding their reason changes how you negotiate. Ask directly: "What decisions are you trying to have input on?" That question alone often reveals whether this is a control issue or a communication issue. Some investors accept observer rights once they articulate their actual concern.

Before taking any investor seriously at seed, review what their past deals signal about how they operate once inside a boardroom. Read about investor red flags that founders often miss before closing a round.

How to Respond to the Request

Get clear first on what they are actually asking for. "Board seat" and "board control" are different things.

If they want a single board seat:

• This is standard at seed and acceptable.

• Keep the board at three seats total through seed and Series A.

• Offer observer rights to other investors as an alternative to additional seats.

If they want majority control or co-equal seats:

• Ask which specific decision they feel exposed on.

• Offer monthly reporting and information rights as an alternative to a formal seat.

• Push for a sunset clause that resets board terms at your next round.

If they will not move:

• Walk away seriously, not as a tactic.

• Founders who accept majority investor control at seed rarely reclaim it without a full buyout or legal dispute.

Negotiating Board Composition

When structuring the board, keep these specifics in mind:

• Keep total seats odd to avoid deadlocks (3 or 5 seats).

• Push for an independent seat you both agree on, rather than a second investor seat.

• Define voting thresholds for key decisions, including acquisitions, new equity issuance, and the sale of the company.

• Include founder protection clauses covering removal, dilution, and key-man provisions.

One move founders often miss: propose a board observer seat with no voting rights. Many investors accept this because it gives them visibility without a control standoff.

Understanding startup defensibility helps you recognize when you have real leverage in these conversations versus when you are negotiating from a weak position.

What the Request Signals About the Investor

An investor who insists on board control at seed is telling you something about how they plan to operate. The request itself is not always disqualifying. How they respond to pushback usually is.

An investor who listens, explains reasoning, and accepts a reasonable compromise is worth keeping in the conversation. One who treats majority control as non-negotiable on a $500K check is probably not the right partner for the difficult years ahead.

Read about what causes investors to delay decisions after initial interest to understand how your behavior during term negotiations shapes their confidence in you.

The Bottom Line

Board control at the seed stage is negotiable. Most investors do not expect majority seats. Those who demand them often have a history worth researching before you sign anything.

Protect the odd-numbered board structure, push for observer seats as an alternative to additional voting seats, and treat the negotiation itself as a signal about the relationship ahead.

SheetVenture helps founders research investor board history and deal terms before negotiations start, so you walk in knowing exactly what leverage you have.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active