VC deal appetite shifts dramatically across fund lifecycle stages. Learn four stages and how to time outreach for maximum conversion.

A VC firm's appetite for new deals changes dramatically depending on where it sits in its fund lifecycle: early deployment periods favor aggressive new investment, mid-cycle periods balance new deals with portfolio support, late-cycle periods shift almost entirely toward reserve management, and fundraising periods create temporary paralysis that most founders never anticipate.

The firm's website looks identical at every stage. The deal appetite is not.

Why Fund Lifecycle Creates Invisible Barriers

What understanding lifecycle stage enables:

Targeting firms in active deployment windows rather than reserve management mode

Interpreting slow investor behavior as lifecycle friction rather than disinterest

Timing outreach to coincide with new fund closes when appetite resets completely

What ignoring lifecycle stage causes:

Spending weeks in conversations with firms structurally unable to write new checks

Missing the window when a newly closed fund is actively hunting deals to deploy

For deeper context, understand active investor signals and why deployment status matters more than stated thesis when evaluating whether a firm will actually move.

The Four Lifecycle Stages and What Each Means for Deal Appetite

1. Early Deployment: Months 1 to 18 After Fund Close

What this looks like: The firm has fresh capital and LP pressure to deploy consistently. Partners are actively sourcing, response rates are higher than at any other stage, and the firm is willing to take more risk on earlier companies because reserves have not yet been committed to existing portfolio needs.

What founders experience: Faster responses, more first meetings, and greater willingness to lead rounds. This is the highest-conversion window in a fund's life.

2. Mid-Cycle Deployment: Months 18 to 36

What this looks like: The firm has deployed 40 to 60% of the fund. New deals compete directly with reserve allocation for existing portfolio companies. Deal quality thresholds rise because the firm is becoming more selective with remaining capital.

What founders experience: Longer response times, more diligence depth before conviction forms, and greater emphasis on traction proof rather than thesis fit alone.

Learn how investors react to slow versus fast fundraising processes and how lifecycle position explains behavior that looks like disinterest from the outside.

3. Late-Cycle Reserve Management: Months 36 to 60

What this looks like: The firm has deployed 70 to 85% of the fund and holds remaining capital primarily for follow-on investments. New deals happen rarely and only when exceptional enough to justify reducing reserves below target ratio.

What founders experience: Polite but non-committal responses, requests to stay in touch, and timelines that extend indefinitely without explanation.

4. Fundraising Period: Variable Timing

What this looks like: The firm is raising its next fund and has entered a de facto pause on new investments. Most firms in active fundraising slow new deal activity to near zero.

What founders experience: Partner enthusiasm in meetings that never converts to a term sheet, with vague references to timing that obscure the real constraint.

Red flag: A firm publicly announcing a new fund raise is simultaneously the most exciting and least actionable firm on any target list.

Lifecycle Position by Observable Signal

Lifecycle Stage | Observable Signal | Data Source | Outreach Priority |

|---|---|---|---|

Early Deployment | New fund close announced in last 18 months | SEC Form D, press releases | Highest: move immediately |

Mid-Cycle | Last fund close 18 to 36 months ago, active deal flow | Crunchbase deal history | Medium: strong pitch required |

Late Reserve | No new deals announced in 6 or more months | Portfolio page update frequency | Low: wait for next fund |

Fundraising Period | Partners referencing new fund publicly | LP announcements, partner interviews | Pause: re-engage at close |

New Fund Imminent | Active LP roadshow signals in trade press | VC media, conference appearances | Prepare: position for close |

The pattern: Every lifecycle signal is discoverable through public sources before the first email is sent. Founders who check fund age before building outreach lists consistently prioritize higher-conversion conversations.

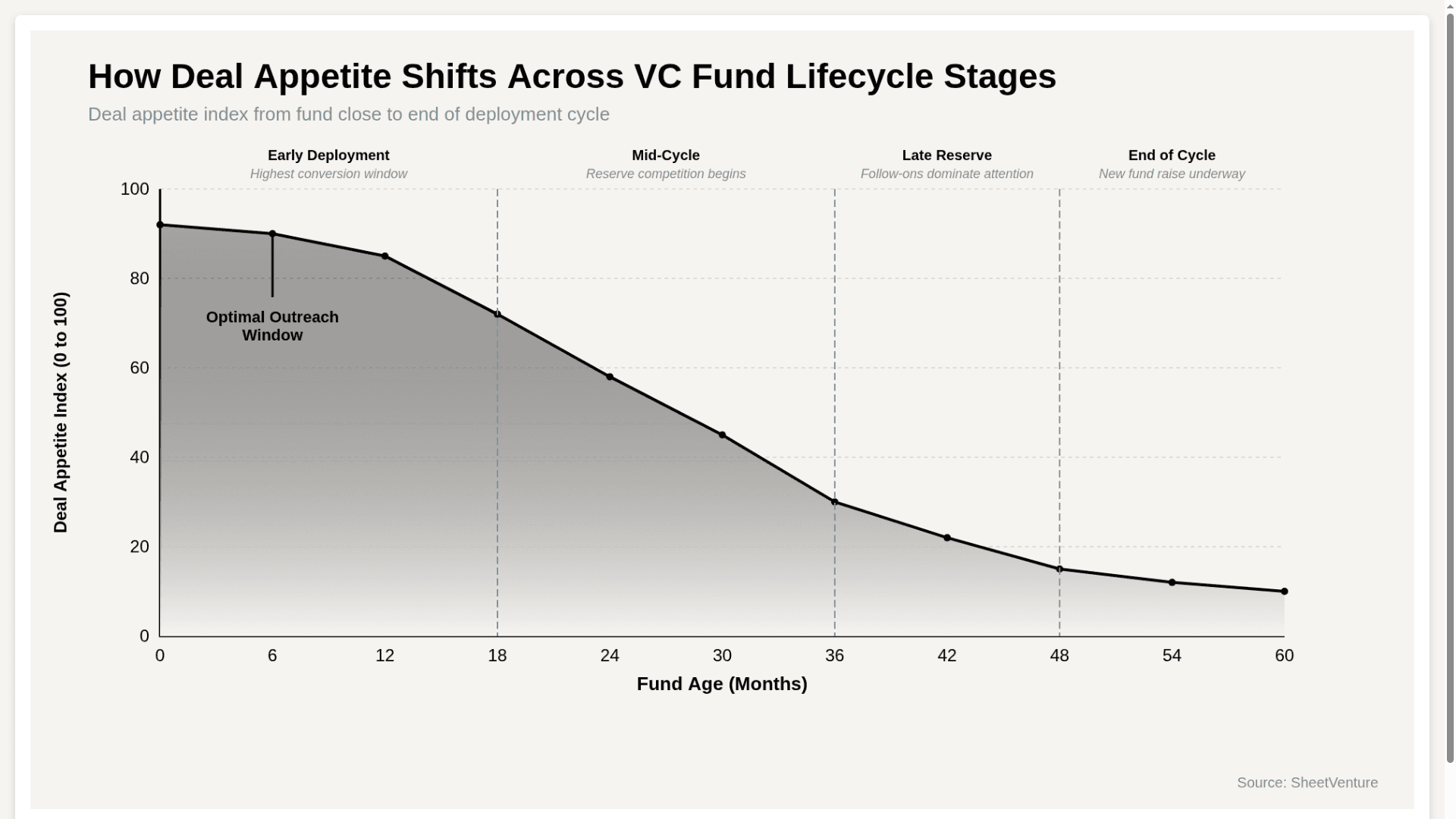

Deal Appetite Index Across Fund Lifecycle Stages

The chart shows deal appetite drops by more than 80 points across a full fund lifecycle, confirming that the same pitch to the same firm produces dramatically different outcomes depending entirely on when the conversation happens.

How to Research Lifecycle Position Before Outreach

Check SEC Form D filings to find the exact close date of the firm's current fund

Review Crunchbase deal history for pace of new investments in the last six months

Search for LP roadshow signals or new fund announcements in trade press

The principle: Fund lifecycle position is public information that most founders never look up. The research takes 15 minutes per firm and changes the entire outreach priority calculation entirely.

Use investor intelligence to identify which firms have closed funds in the last 18 months and are actively deploying right now.

The Bottom Line

Fund lifecycle stage affects deal appetite through four distinct phases: early deployment where appetite is highest and conversion is fastest, mid-cycle where reserve competition slows decisions, late-cycle where follow-ons dominate partner attention, and fundraising periods where new investment effectively pauses.

Research fund age before building any outreach list. Prioritize firms in early deployment. Deprioritize firms in reserve management or active fundraising. Timing the firm matters as much as fitting the thesis.

SheetVenture helps founders identify which firms are in active deployment right now so every conversation starts with a firm that is structurally able to write a check.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active