LP capital calls decide when VCs actively write checks. Learn how fund deployment timing shapes your entire raise.

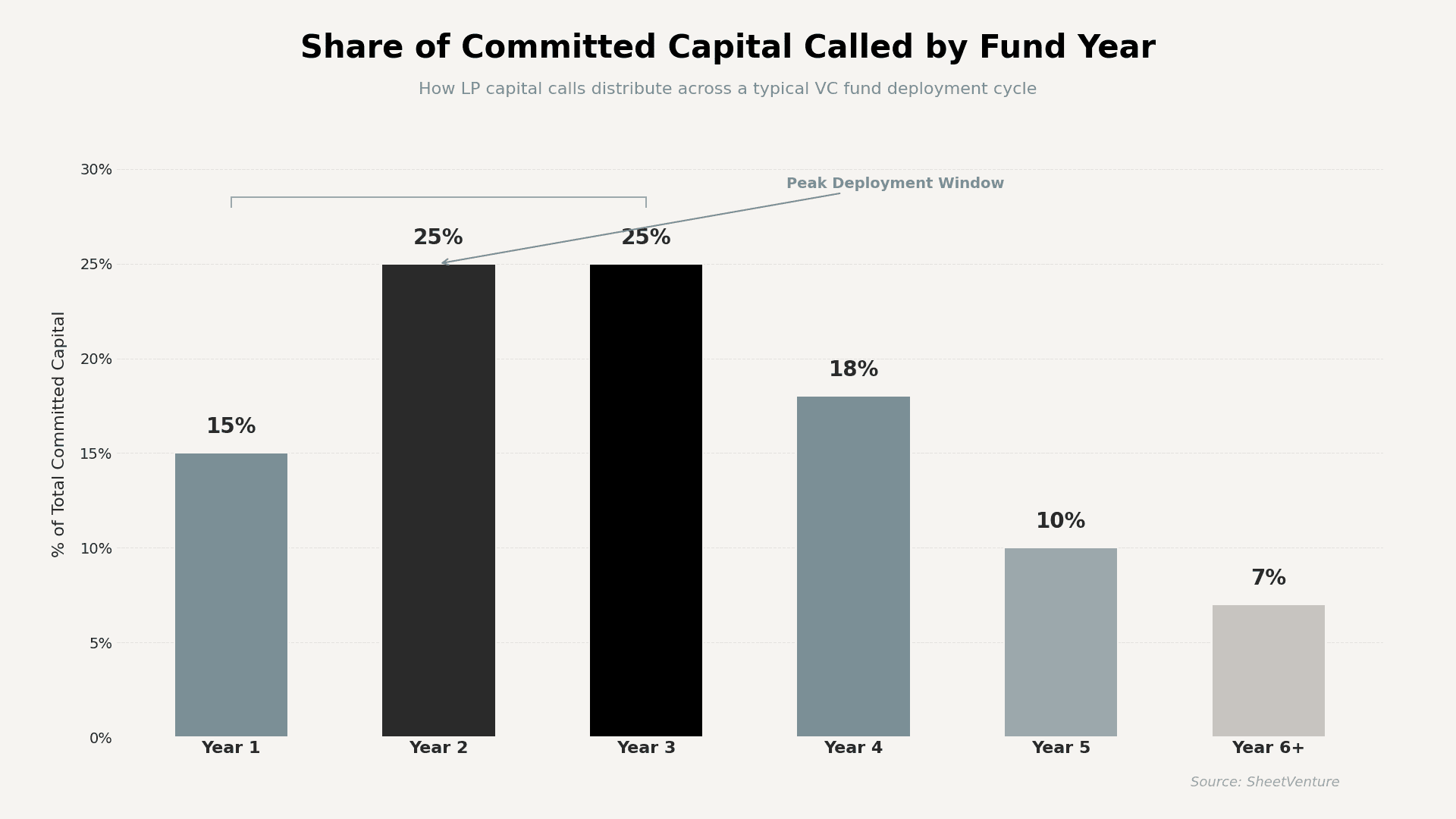

LP capital calls directly control when VC firms can write checks. Most venture funds deploy 60–70% of committed capital within the first three years, with Years 2 and 3 representing peak activity. When LPs delay calls or macro conditions slow new commitments, deployment windows shrink, and investors become far more selective.

A VC partner might love your company, but physically cannot invest if the fund hasn’t called capital from its LPs yet. The capital call schedule is the hidden clock behind every firm’s deal activity.

What Are LP Capital Calls and How Do They Work?

When a VC fund closes, LPs (pension funds, endowments, family offices) don’t wire the full commitment upfront. The GP issues capital calls, formal requests for LPs to transfer a portion of pledged capital as deals materialize.

• A $200M fund might call 15–20% in Year 1, then 25% annually in Years 2–3.

• Calls happen quarterly or as deals close, not on a fixed calendar.

• The GP can’t deploy what hasn’t been called, so deal pacing depends entirely on call timing.

Founders who know which firms carry dry powder gain a direct edge in targeting active investors.

How Does the Capital Call Cycle Affect VC Deal Activity?

Capital calls create a predictable rhythm inside every fund. Early on, GPs build their portfolio and call capital aggressively. Later, the pace slows as remaining capital is reserved for follow‑on rounds in existing portfolio companies.

Capital Call Deployment by Fund Year

Fund Year | Capital Called (%) | Primary Use | New Deal Pace | Founder Relevance |

Year 1 | 10–15% | First investments, thesis testing | Moderate (3–5 deals) | Good window if thesis fits |

Year 2 | 20–25% | Core portfolio building | High (6–10 deals) | Best window for new pitches |

Year 3 | 20–25% | Portfolio rounding + follow‑ons | High (5–8 deals) | Strong, but slots are filling |

Year 4 | 15–20% | Follow‑on heavy | Low (2–4 deals) | Harder to break in |

Year 5+ | 7–15% | Reserves, bridge rounds | Minimal (0–2 deals) | Very low new deal activity |

The difference between pitching a fund in Year 2 versus Year 5 is enormous. By Year 4, most funds have allocated 75–80% of capital. Confirm VCs are actively investing before spending weeks on outreach.

When Are VC Firms Most Active in Deploying Capital?

Peak deployment falls between months 12 and 42 after final close. During this stretch, GPs face pressure to put committed capital to work. Sitting on uncalled capital too long raises LP questions about whether the fund can deliver returns.

• Years 2–3 account for roughly 50% of total capital deployment.

• GPs who deploy too slowly risk LP pushback on future fundraising.

• When a firm announces a new fund, expect 6–12 months before peak deal flow begins.

How Do Delayed Capital Calls Impact Startups Seeking Funding?

When macro conditions tighten, LPs slow commitments. Interest rate hikes, public market corrections, and the denominator effect (when other asset classes drop, making VC allocations look too large) cause LPs to pull back. This creates a downstream drought for startups.

LP Delay Triggers and Downstream Startup Impact

Trigger Event | LP Response | VC Fund Impact | Startup Effect |

Interest rate hikes | Slower new fund commitments | Smaller fund sizes, longer closes | Fewer new checks written |

Public market correction | Denominator effect rebalancing | LPs reduce allocations | Existing funds slow deployment |

LP liquidity crunch | Delayed capital call fulfillment | GP pauses new deals | Term sheets delayed or pulled |

Geopolitical uncertainty | Risk‑off posture | Reserves prioritized over new deals | Seed/Series A hardest hit |

The 2022–2023 correction proved this. LP commitments to venture dropped 35% year over year, and finding active VCs became the most important variable in fundraising success.

What Should Founders Watch for in VC Fund Timing?

You can’t ask a partner how much capital they have left. But you can read the signals.

• Track fund announcements: A fund closed 6–18 months ago is your best target.

• Watch deal pace: 8+ investments this year signal active deployment.

• Check SEC filings: Form D shows recent fund sizes and closing dates.

• Avoid funds older than 4 years unless they’ve announced a new vehicle.

Use SheetVenture to surface real‑time data on which firms are in active deployment windows, so you stop pitching funds that can’t write new checks.

The Bottom Line

LP capital calls are the invisible infrastructure behind VC investing. They determine when capital enters the fund, how quickly GPs deploy, and how selective investors become at each stage. Most founders pitch without knowing where a fund sits in its cycle, and that blind spot costs months of wasted outreach. Target funds in Years 1–3. Watch for new fund announcements. The money has to exist before it can reach you.

SheetVenture helps founders identify which funds are in active deployment, so every pitch goes to an investor who can actually write a check.

Last Update:

Everything you need to understand private markets

Understand your market in real-time.

Filter by stage, sector, and exact geography.

Access 30,000+ verified, daily-updated active